Tuesday, December 10, 2019

Housing Market in Cyprus

From the IMF’s latest report on Cyprus:

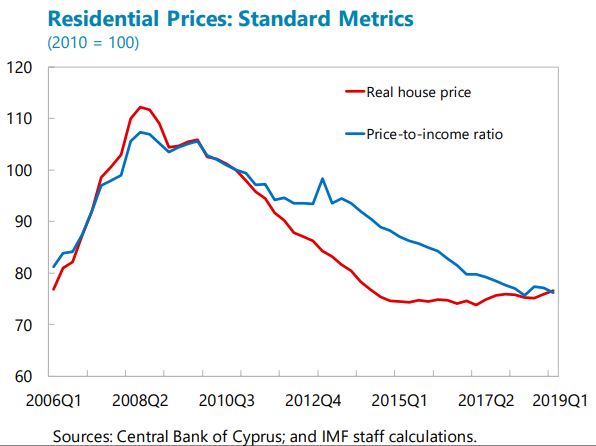

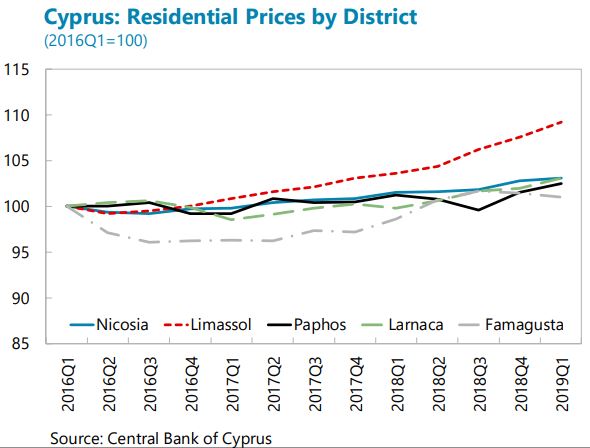

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented, however, with higher price increases observed primarily in a growing luxury segment in some coastal areas (e.g., Limassol), fueled by the CIP-linked demand from non-residents, with limited spillovers to other segments so far. Rents have been rising rapidly—17 percent in 2018— mainly driven by the growing demand from foreign students and lagging supply of rental property investments, prompting the authorities to increase rental and housing subsidies and a range of incentives for developers to increase supplies of affordable housing and rental properties.

Macro-financial risks from the property market appear limited now but warrant close monitoring. While the sales of repossessed collateral properties by banks and CACs could potentially depress prices, downward pressures from such sales have not been evident in any market segments. However, it is important to continue monitoring sectoral and regional real estate market developments, considering the segmented nature of the market. Macroprudential measures tailored to the market segment should be undertaken if warranted, e.g. if the luxury sales become associated with rapid credit growth or high loan-to-value ratios. On the supervisory front, continued monitoring is needed on the large holdings of repossessed real estate by banks and CACs, to discourage and limit the risk of excessive holding of foreclosed properties. Also, the increased real estate holding by investment funds warrants close monitoring to mitigate risks related to liquidity mismatches. Supervisory tools, in particular Pillar 2 requirements and explicit bank-specific objectives, should continue to be used to discourage excessive holding of foreclosed properties by banks.”

Posted by at 11:01 AM

Labels: Global Housing Watch

Subscribe to: Posts