Tuesday, June 25, 2019

Assessing House Prices in Canada

From the IMF’s latest report on Canada:

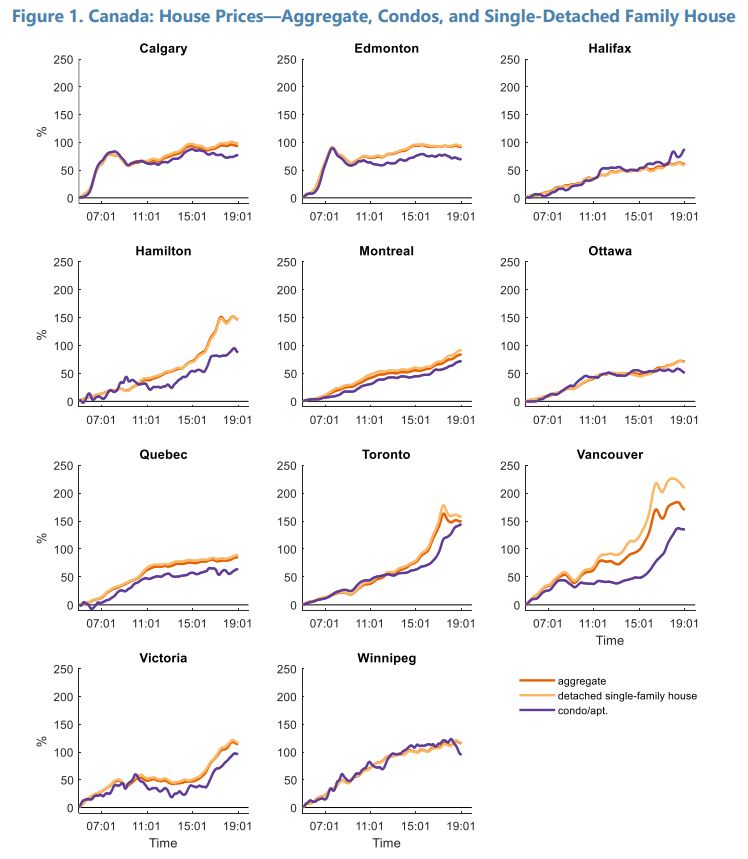

“House prices in most Canadian regions can be explained by economic fundamentals, but prices in Hamilton, Toronto, and Vancouver are currently well-above estimated attainable levels. Since 2000, house price developments in most metropolitan regions can be explained by robust income growth and a decline in mortgage interest rates. House prices have broadly increased in line with households’ borrowing capacity. However, since 2015, prices in Hamilton, Toronto, and Vancouver have deviated significantly from fundamentals. By the end of 2018, pricing gaps stood at around 50 percent for Toronto and Vancouver, and almost 60 percent for Hamilton.

The overvaluations currently observed in Hamilton, Toronto, and Vancouver are not unprecedented. In 2006, house prices in Calgary and Edmonton increased sharply above estimates of borrowing capacity. Pricing gaps normalized by 2012 due to a combination of moderate declines in house prices, strong household income growth, and a decline in interest rates. Looking ahead, housing markets in Hamilton, Toronto, and Vancouver are not likely to benefit from such significant declines in interest rates. This suggests that without very strong income growth, there is a risk of further price corrections in these markets.

Nationwide increases in price-to-income ratios have significantly lowered housing affordability. Declines in mortgage rates have generally been rapidly priced in by housing markets, increasing price-to-income and loan-to-income ratios. With rising price-to-income ratios, down payments have become larger, increasing the time it takes to save for a house, and adversely impacting housing affordability. While housing affordability has deteriorated in all of the regions examined, the deterioration has been most marked in Hamilton, Toronto, and Vancouver.

If house prices rapidly reflect households’ ability to borrow, even well-intentioned policies that improve access to credit are likely to increase house prices and adversely impact affordability. Policy measures that increase households’ capacity to borrow—such as increasing the mortgage loan amortization period or subsidizing loans—will likely put additional upward pressure on prices. Indeed, for such measures to work, the supply of housing would need to be exceptionally (and unrealistically) elastic, even in the short run. As such, policy measures focused on increasing housing supply are needed to durably improve housing affordability over the long term.”

Posted by at 3:51 PM

Labels: Global Housing Watch

Subscribe to: Posts