Monday, May 13, 2019

Housing Market in Luxembourg

From the IMF’s latest report on Luxembourg:

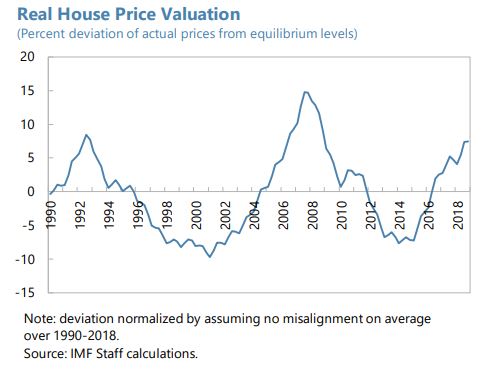

“Real house prices are estimated to be slightly overvalued in 2018. The percent deviation between the actual house price index and the predicted house price index suggests that real house prices were slightly overvalued, by about 7.5 percent in 2018.

Going forward, given supply constraints, Brexit-related immigration flows could add demand pressures and increase overvaluation of residential real estate (RRE) prices.

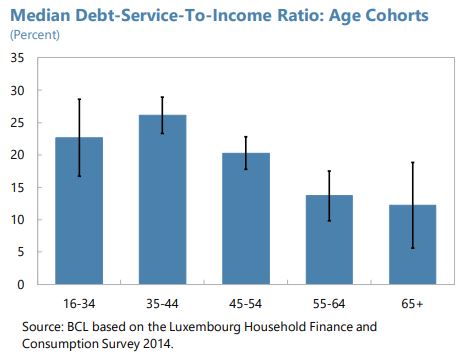

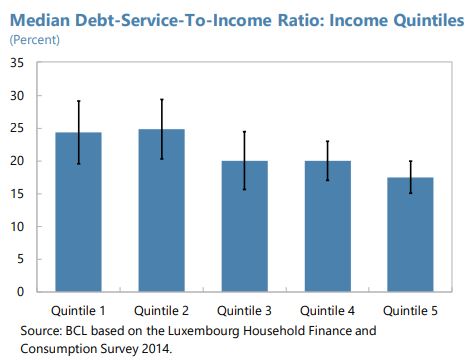

However, elevated household indebtedness indicates medium-term vulnerabilities, especially among younger age cohorts. Household debt remained high at about 170 percent of net disposable income in 2017, placing Luxembourg above the average of OECD countries. According to the latest available data from CSSF, 32 percent of households have a debt-service-to-income (DSTI) ratio greater than 45 percent. Disaggregated data from Household Finance and Consumption Survey (2014) indicates very high debt-to-income and DSTI ratios for younger cohorts (below 45 years old). The median and 75th percentile DSTI ratios were approaching 25 and 40 percent of disposable income, respectively. Classified by income quintiles, debt service burden is larger for poorer households (quintiles 1 and 2). In 2018, the share of adjustable rate mortgages in new mortgages remained stable at about 50 percent, indicating that some household balance sheets remain vulnerable to interest rate risks. These vulnerabilities would be exacerbated should monetary policy normalize faster than anticipated.

Rising RRE prices and elevated household indebtedness require continued monitoring of financial stability risks including banks’ ability to absorb price declines. Non-performing loans (NPLs) in the real estate sector remain low, with the ratio of total NPLs in RRE to total assets of the domestic banking system at 0.18 percent. However, borrower-based indicators point towards the need for closer monitoring of financial stability risks. Loan-to-value (LTV) ratios above 80 percent, for instance, are high at 31 percent of the outstanding mortgage stock. This is expected to increase further as one half of all new mortgage loans continue to have LTV ratios above 80 percent.”

Posted by at 10:40 AM

Labels: Global Housing Watch

Subscribe to: Posts