Tuesday, March 12, 2019

Housing Market in Belgium

From the IMF’s latest report on Belgium:

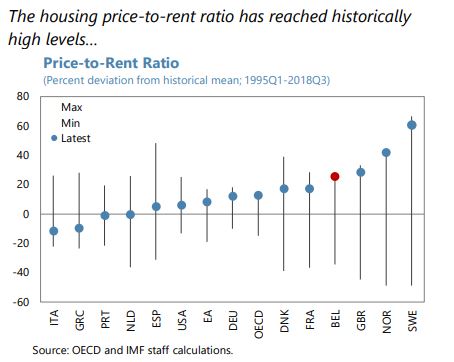

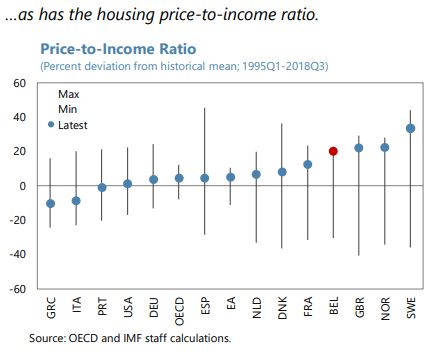

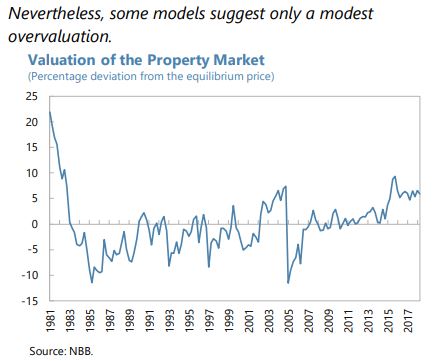

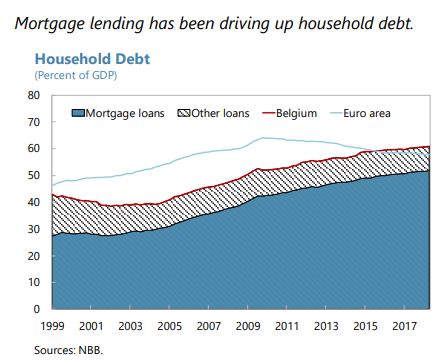

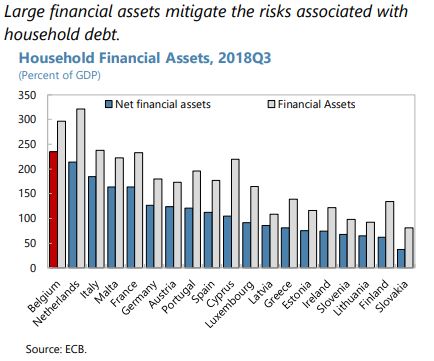

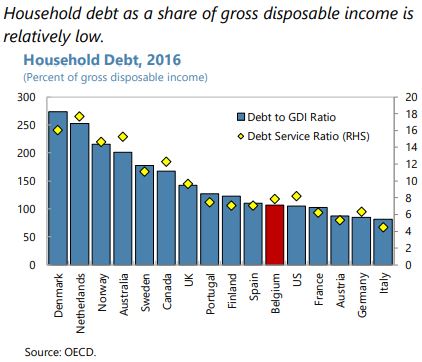

“Private sector indebtedness, primarily associated with household debt, and sustained increases in housing prices pose additional challenges. Strong growth in mortgage lending (9 percent in 2018) has contributed to a sizeable increase in household debt and housing prices. Models, however, point to only a modest house price overvaluation, depending on location. Meanwhile, the share of loans with a loan-to-value (LTV) ratio below 80 percent has declined by about 10 percentage points during 2014–2017. Although default rates are currently low, households have substantial assets in the aggregate, and household debt-to income is in line with peers, a sharp housing (and asset) price correction could result in rising defaults for some groups of the population and affect banks’ solvency, with second round effects on investment, consumption, and growth. 12 Belgian unconsolidated corporate debt has also increased over the last few years to a relatively high level, although, the level is more in line with peers after accounting for intragroup loans. Nonetheless, its dynamics warrant close monitoring, given recent strong bank credit growth to the corporate sector (…).

Staff welcomed the authorities’ recent macroprudential measures to address risks in the housing market and encouraged the authorities to remain proactive. To guard against a correction in housing prices and discourage banks from taking excessive credit risk, the National Bank of Belgium (NBB) introduced in May 2018 an add-on to risk weights on bank mortgage exposures as a new macroprudential measure. In view of the robust overall level of credit growth (5.9 percent in 2018) and credit gap (the NBB estimates this at 2 percent at end Q3-2018), staff recommended that the NBB continue to closely monitor the build-up of cyclical risks in both the household and corporate sectors and stand ready to tighten macroprudential policy further, including through the use of a countercyclical capital buffer. The authorities could also consider revising the framework for macroprudential decision-making to ensure the ability to deploy a broader range of macroprudential policies in a timely manner, as recommended by the 2017 Financial Sector Assessment Program (FSAP) mission.”

Posted by at 9:26 AM

Labels: Global Housing Watch

Subscribe to: Posts