Tuesday, February 19, 2019

The forecasting record

From a new post:

“The ONS says GDP grew by 1.4% last year. 1.4% is a significant number: it is exactly what the private sector economists surveyed by the Treasury predicted in December 2017 that growth would be in 2018.

Granted, this bulls-eye might not survive future revisions to GDP estimates. But it reminds us that economists’ forecasts for growth are often not too bad.

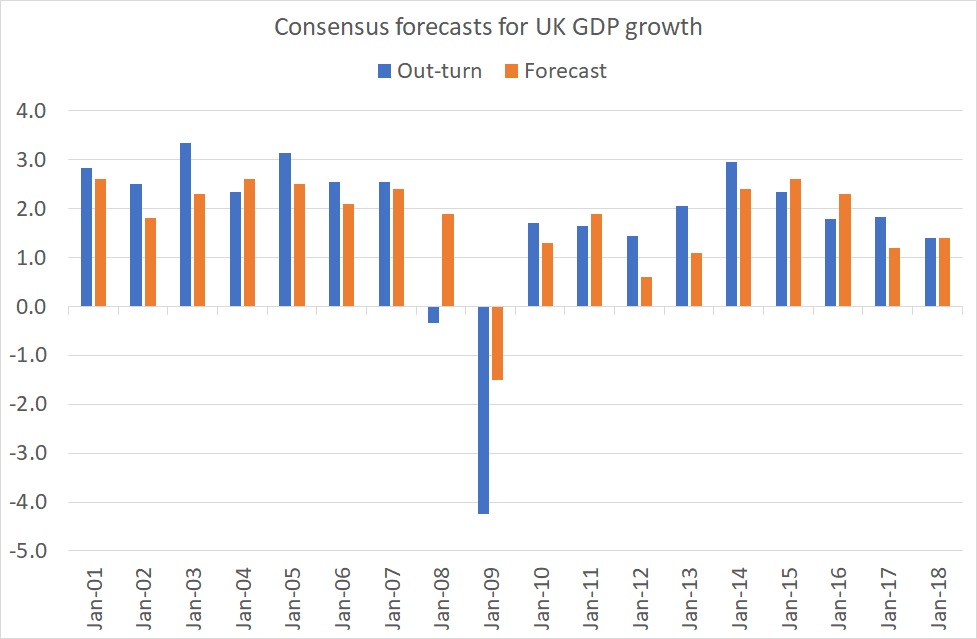

My chart shows the point. It compares forecasts made in December for growth the following year to actual growth since 2001. Most of the time, the forecasts aren’t too far out. Where they go badly wrong is in recessions. Economists don’t see these coming. In December 2007 they forecast that GDP would grow 1.9 per cent in 2008. In fact it shrank. And even in December 2008 – after the banking crisis – they grossly under-predicted the depth of the recession.

This fitted the pattern. Back in 2000 Prakash Loungani wrote:

The record of failure to predict recessions is virtually unblemished. Only two of the 60 recessions that occurred around the world during the 1990s were predicted a year in advance. That may seem like a tough standard to impose on forecast accuracy. Maybe so—but two-thirds of those recessions remained un-detected seven months before they occurred.

In December 1990, for example, UK economists forecast growth of 0.3% in 1991. In fact, we got a 1% drop.

Economic forecasts, then, are reasonably OK except when we really need them.

Why? One possibility, suggested by Loungani, is that economists are slow to update their forecasts in light of news. One bit of evidence for this is that they also under-predicted the boom of 1988 (probably because they over-estimated the adverse effect of the 1987 stock market crash). Another possibility is that mainstream forecasters lack incentives to break with the consensus and predict recessions: it’s better to be wrong in a crowd. It’s for this reason that it is mavericks and those wanting to make a name for themselves who predict doom.

I suspect, though, that there’s something else. It’s that recessions are caused by things which are hard for macroeconomists to discern. For example, Xavier Gabaix shows how they can be caused by failures at large firms. And Daron Acemoglu and colleagues have described how they can be amplified by network effects: trouble at a firm at the centre of a hub can spill over into other firms whereas trouble at a spoke does not. These are both part of the story of the 2008-09 crisis.

Macroeconomists are tolerably good at predicting fluctuations in aggregate demand. It is other things – such as supply shocks, network and peer effects or banking crises – they’re not so good at foreseeing.

It doesn’t automatically follow, however, that recessions are wholly unpredictable. US evidence strongly suggests that inverted yield curves lead (with a variable lag) to economic downturns. I suspect this is for the same reason that consumption-wealth ratios help predict bad times. It’s because such data aggregates the dispersed and fragmentary knowledge of countless individuals. There some specific conditions when the wisdom of crowds works better than experts.”

Posted by at 10:51 AM

Labels: Forecasting Forum

Subscribe to: Posts