Monday, February 18, 2019

A Look at Housing, Mobility and Welfare

Global Housing Watch Newsletter: February 2019

In this interview, Gabriela Inchauste talks about Living and Leaving: Housing, Mobility and Welfare in the European Union—a new report from the World Bank. Inchauste is a Lead Economist in the Poverty and Equity Global Practice of the World Bank.

About the report…

Hites Ahir: What prompted you and your team to write this report?

Gabriela Inchauste: The main motivation for the report came from our concern over the growing divides in the European Union, with widening productivity gaps and growing inequality in labor incomes. The divide often plays out across regions within countries, as high-productivity jobs are concentrated in metropolitan regions. We wondered the extent to which these divides can be explained by the housing market. To the extent that households in the European Union hold most of their wealth in the form of illiquid and immovable assets such as land and housing, they can be an important source of wealth inequality and can also determine intergenerational mobility if homeowners are anchored to the localities where they live, independently of how prosperous or dynamic those locations are. This is problematic from a growth perspective because it implies that the labor force is not moving to where it can be most productive. For young people and for newcomers, housing affordability can be a real barrier to accessing good jobs, and therefore a key determinant of individual well-being and overall economic growth. Our main goal was to unravel the combined impacts of housing policies and regulations on household welfare.

Hites Ahir: What are the main findings of the report?

Gabriela Inchauste: There are three main findings. First, the most productive metropolitan areas are precisely the places where lack of affordable housing is most acute, effectively shutting out tenants, newcomers and the youth from good job opportunities, thus limiting growth and inclusion.

Second, if higher housing prices today don’t lead to more houses built in the future, then housing affordability is more prevalent. The differences in the responsiveness of housing supply to increases in housing prices varies widely across European Union countries: those with low responsiveness have more severe housing affordability constraints. Stricter regulatory environments and weak institutions are associated with low responsiveness of housing supply to increases in housing prices.

Third, tax and spending policies across the European Union have focused on homeownership, with scarce attention and resources devoted to easing the barriers and market restrictions that could improve housing affordability and allow workers to move to where they are most productive. Housing allowances are the most progressive of interventions, particularly when directed at low-income tenants, while mortgage subsidies do not meet the housing needs of the lowest income groups.

Hites Ahir: What are the implications of your findings for policymakers?

Gabriela Inchauste: The report highlights three areas for attention. First, create enabling conditions to allow the housing supply to expand. Overly restrictive land use and development regulations constrain housing growth and drive up prices. Cities could encourage new construction or the redevelopment of existing structures by permitting appropriate floor-space ratios, building heights, and density in specific target zones. Cities can also streamline their processes to speed up land-use approval and permitting, creating a more predictable and less burdensome process. In some member states, improving property rights and the land administration system is a priority. Finally, developing governance structures that ensure efficient coordination mechanisms across financing, urban planning, infrastructure development, land-use regulation, building codes, delivery and contracting approaches is critical.

Second, use public finance more strategically. Governments should emphasize strategic investment projects in greenfield housing as a central part of their investment strategies, together with transportation to facilitate commuting to the centers of economic activity. Moreover, a shift in government spending away from tax and benefit incentives that favor homeownership in favor of tenure-neutral, portable and progressive housing allowances would improve redistribution and efficiency. Similarly, instead of incentives aimed at homeownership for the young, governments could consider providing housing allowances for targeted groups, such as the youth, potentially making benefits conditional on job search responsibilities.

Third, improve monitoring and dissemination of housing data and local-level information. Better monitoring and dissemination of information at the metropolitan level on housing prices, employment, wages, housing policies and regulations, and other indicators would help to inform policy makers. Ideally, local, regional, and national governments should create a publicly available house price registry with information on addresses, sales prices, and quality of housing (energy rating, square meters, and so on), with information as close to real time as possible, in line with other high-income countries. House purchase cost indicators could also be published to benchmark the transaction costs in place at the local, regional, and national levels. This level of transparency could lead to greater competition across jurisdictions and contribute to more efficient, and equitable housing markets.

On residential mobility …

Hites Ahir: What is the current state of mobility in the European Union?

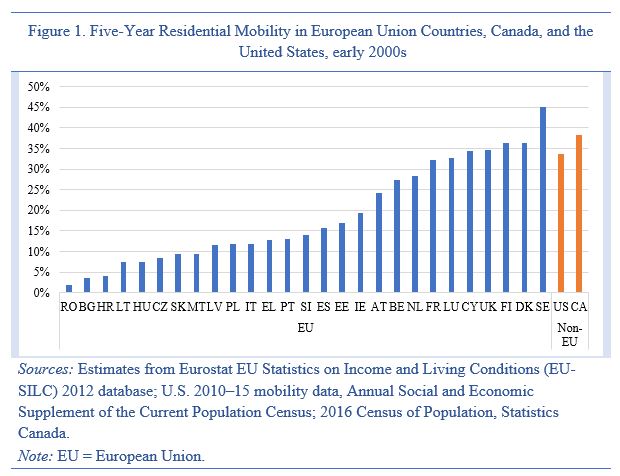

Gabriela Inchauste: Residential mobility is low in the European Union overall compared with Canada and the United States, particularly in Central and Eastern European countries, which could limit agglomeration and increases in productivity. Residential mobility in the report is defined as a change in dwellings and does not include mobility outside their country of origin. Data on five-year residential mobility rates from European Union countries show substantial variations across countries, ranging from 1.8 percent in Romania to 45.1 percent in Sweden (Figure 1)

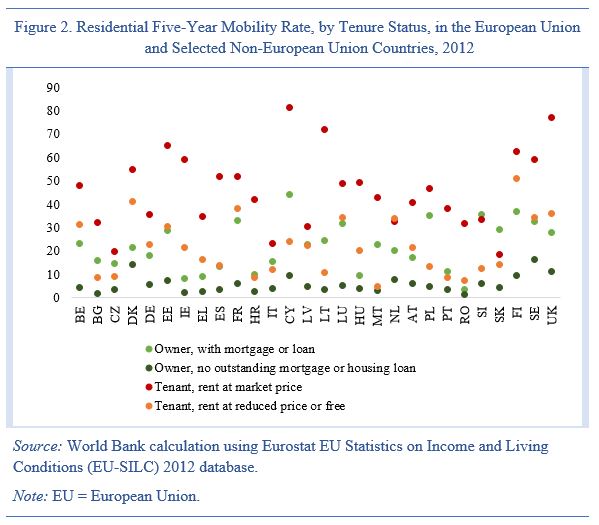

Across all countries, outright homeowners are the least mobile, and tenants paying market rents are the most mobile (Figure 2). Data on intention to move similarly show that residents in Central and Eastern European countries are much less likely to move, on average, than residents of other European Union member states. Notably, among countries with the lowest willingness to move, a large share of those who do intend to move were looking for opportunities abroad. This reflects the large wage differentials with major destination countries in Western Europe and may at least partly explain the lack of internal mobility. Although the decision between external and internal mobility is likely made jointly, especially in the context of free labor mobility within the European Union, we focus on internal mobility primarily because of limited information in the household surveys.

Hites Ahir: Could you discuss how do housing market regulations and institutional factors affect mobility?

Gabriela Inchauste: We estimate the extent to which country-level regulations and policies affect the likelihood of mobility. The types of policies analyzed include rental market regulations (degree of rent control and tenant protection), aggregate transaction costs, and institutional factors that affect the broad functioning of the housing market. In addition, the effect of broader policies influencing housing affordability, such as access to credit and unemployment benefits, are also assessed. We find that higher mobility is associated with lower rent control, tenant protection, and transaction costs. They are also associated with higher access to housing finance, better property rights protection, and better quality of land administration. Institutional factors (that is, weak protection of property rights and low quality of land administration) are closely linked to and negatively affect mobility because they influence the broader functioning of the market. This is an area where the policy direction is unambiguous, and Bulgaria, Croatia, Greece, and Romania could particularly benefit. Finally, we find that institutional factors disproportionately affect the mobility of younger people relative to older people. The mobility of younger people is comparable to or even lower than the mobility of older people in most European Union member countries, though with the caveat that we do not capture external migration in the data.

On policies…

Hites Ahir: In the report, you discuss three types of policies for affordable housing: schemes for home buyers or homeowners, housing allowances, and schemes for tenants. Which is the most effective and why?

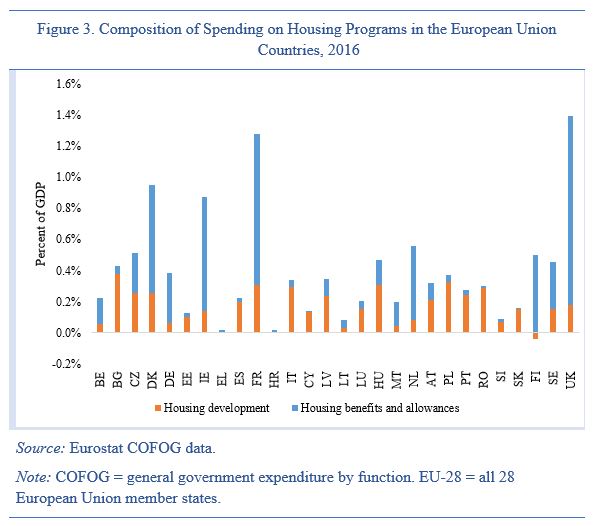

Gabriela Inchauste: The report undertook a stocktaking exercise which identified a total of 208 programs across the 28 European Union member states. The resources dedicated to each type of program vary widely, with France, Germany, Ireland, the Netherlands, and the United Kingdom dedicating more resources to housing allowances, while southern and eastern European Union countries spend much more on housing development (Figure 3).

In terms of the effectiveness of different programs, we found that housing allowances are the most progressive and perhaps the most effective in improving household affordability. About 85 percent of tenant beneficiary households and 60 percent of homeowner beneficiary households on average belong to the bottom 40 percent of the income distribution across countries. However, given the relatively scarce resources devoted to these programs in many countries, a large share of poor households in the European Union still do not receive housing allowances; in fact, less than half of the poorest quintile receives housing allowances in all but 10 European Union member states.

In contrast, tax relief for home buyers and homeowners is expensive and concentrated in the top half of the distribution. In addition, there is an empirical literature that finds that mortgage interest deduction programs that are not targeted to low-income households do not actually increase homeownership but rather induce homeowners to buy larger and more expensive houses, shifting resources away from other more productive assets. Further, there is no causal evidence with respect to the existence of positive externalities associated to owning—as opposed to renting—a home. These findings raise serious doubts about the desirability of tax relief for home buyers and homeowners.

Finally, programs for tenants are less common and usually take the form of subsidies and tax relief for home developers. The stocktaking exercise identified 60 different programs for tenants across 27 European Union member states. In 14 countries these include subsidies and tax relief for housing development, and in 27 countries they included social housing. The supply of new social housing has been declining, while reduced funding for these programs has led to greater focus on targeting poorer households. However, there are some important exceptions to this, with most social housing beneficiaries belonging to the top 60 percent of the distribution in the Czech Republic and the Netherlands. Beyond programs for housing developers and social housing, there are other programs for tenants in the form of tax relief, which are found to be progressive and largely concentrated at the bottom of the distribution in Ireland and Italy, but not so in Portugal and Spain.

Hites Ahir: Of all the countries that you surveyed in this report, is there a country that gets housing right?

Gabriela Inchauste: I was especially impressed with housing policies in Ireland, where there are relatively high levels of housing affordability. Ireland has relatively low tenant protection, low transaction costs, high quality land administration and property rights protection and consequently relatively higher mobility. In terms of fiscal policy tools, Ireland has highly progressive housing allowances, to which they dedicate a relatively high share of resources. There are also social housing programs which mostly provide rental accommodation at reduced rates to low income households. Perhaps the only thing I would change is their mortgage interest tax deduction, which mostly benefits the top of the distribution.

Posted by at 8:00 PM

Labels: Global Housing Watch

Subscribe to: Posts