Tuesday, December 11, 2018

Drivers of commodity price booms and busts in the long run

From a VoxEU post by David Jacks, and Martin Stuermer:

“There is a lack of consensus on the importance of various drivers of long-run commodity prices. This column analyses a new dataset of prices and production for 15 commodities, including metals, agricultural goods, and soft commodities, between 1870 and 2015. Demand shocks due to rapid industrialisation and urbanisation have driven a substantial amount of variation in commodity price booms. While demand shocks have gained importance over time, commodity supply shocks have become less relevant.

Understanding the drivers of commodity price booms and busts is of first-order importance for the global economy. A significant portion of real income and welfare in both commodity-consuming and commodity-producing nations hinges upon these prices (Bernanke 2006). They vitally affect the distribution of income within particular nations as the ownership of natural resources varies widely, potentially setting the stage for civil conflict (Dube and Vargas 2013). And the long-run drivers of commodity prices have serious implications for the formation and persistence of growth-detracting and growth-enhancing institutions (van der Ploeg 2011).

But for all this, outside spectators – whether they are academics, the general public, the investment community, or policymakers – remain divided in assigning the importance of various forces in the determination of commodity price booms and busts. Understanding which shocks drive these events and how long they persist is important for the conduct of macroeconomic policy, formulating environmental and resource policies, and, perhaps most importantly, investment decisions in the resource sectors of the global economy.

While the literature on modelling oil markets has examined a handful of booms and busts since the early 1970s (e.g. Kilian 2009, Kilian and Murphy 2014), our analysis of commodity markets is based on a new dataset of real prices and output for 15 grains, metals, and soft commodities from 1870 to 2015 (Jacks and Stuermer 2018). Unanticipated changes in world demand affect all commodity prices simultaneously. Throughout history, aggregate commodity demand shocks due to rapid industrialisation and urbanisation have driven commodity price booms. China’s recent effect on commodity markets is, thus, not a new phenomenon.

Commodities in the long run and identifying price shocks

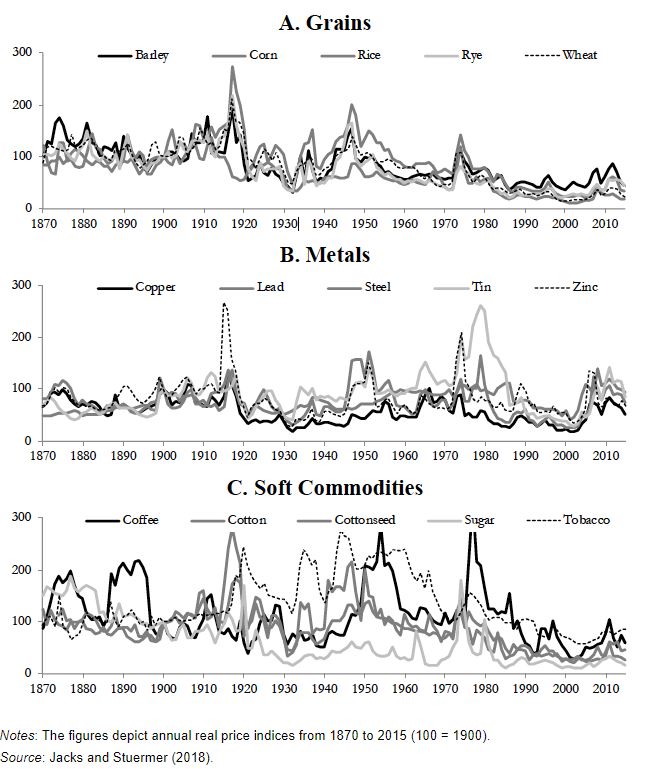

A new dataset encompassing global output and real prices for 15 commodities – barley, coffee, copper, corn, cotton, cottonseed, lead, rice, rye, steel, sugar, tin, tobacco, wheat, and zinc – has been assembled covering the past 145 years (see Figure 1) and representing in excess of $2.5 trillion in annual gross value of production in 2015. The commodity markets selected exhibit characteristics that make such long-run analysis feasible: a high degree of product homogeneity, long-standing evidence of an integrated world market, and no indication of sudden changes in how the commodity is used. Thus, they have desirable characteristics that commodities such as crude oil or iron ore have only gained relatively recently.

Figure 1 Booms and busts are not new phenomena

Continue reading here.

Posted by at 9:59 AM

Labels: Energy & Climate Change

Subscribe to: Posts