Friday, November 16, 2018

Superstar Firms and Cities

From Conversable Economist:

“Imagine two people who have seemingly equal skills and background. They go to work for two different companies. However, one “superstar” company grows much faster, so that wages and opportunities in that company also grow much faster. Or they go to work in two different cities. One “superstar” urban economy grows much faster, so that wages and opportunities in that city also grow faster.

Of course, such patterns of unequal growth have always existed to some extent. When evaluating a potential employer or location choice, people have always taken into account the potential for joining a superstar performer. The interesting question is whether the gap between superstar and ordinary firms, or between superstar and ordinary cities, has been growing or changing over time. For example, some argue that the rise of superstar firms, and the resulting rise in between-firm performance and labor compentiation, can explain most of the rise in US income inequality.

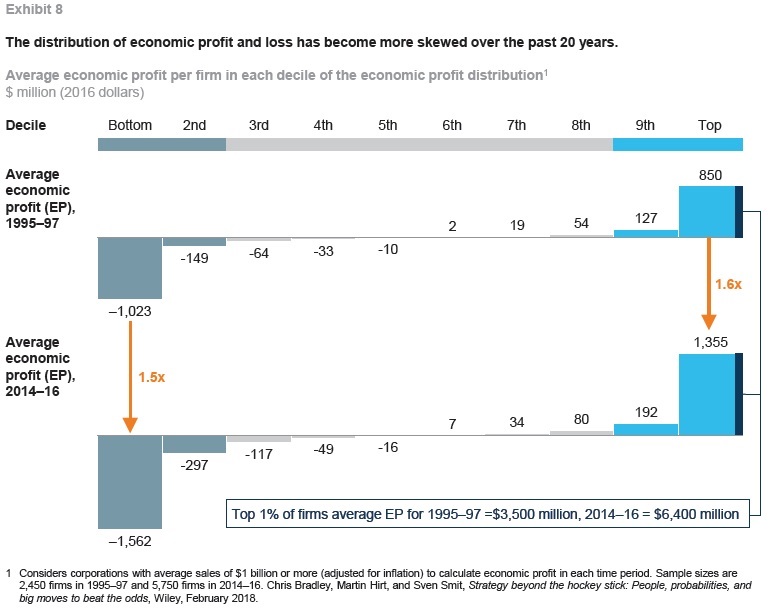

The McKinsey Global Institute has a nice report summarizing past evidence and offering new evidence of their own in Superstars: The Dynamics of Firms, Sectors, and Cities Leading the Global Economy(October 2018). It’s written by a team led by James Manyika, Sree Ramaswamy, Jacques Bughin, Jonathan Woetzel, Michael Birshan, and Zubin Nagpal. Short summary: Superstar firms and cities do seem to be widening their economic leadership gap, with the evidence that certain sectors are superstars seems weaker.

For superstar firms, the report notes:

“For firms, we analyze nearly 6,000 of the world’s largest public and private firms, each with annual revenues greater than $1 billion, that together make up 65 percent of global corporate pretax earnings. In this group, economic profit is distributed along a power curve, with the top 10 percent of firms capturing 80 percent of economic profit among companies with annual revenues greater than $1 billion. We label companies in this top 10 percent as superstar firms. The middle 80 percent of firms record near-zero economic profit in aggregate, while the bottom 10 percent destroys as much value as the top 10 percent creates. The top 1 percent by economic profit, the highest economic-value-creating firms in our sample, account for 36 percent of all economic profit for companies with annual revenues greater than $1 billion. Over the past 20 years, the gap has widened between superstar firms and median firms, and also between the bottom 10 percent and median firms. … The growth of economic profit at the top end of the distribution is thus mirrored at the bottom end by growing and increasingly persistent economic losses …”

Continue reading here.

Posted by at 10:03 AM

Labels: Global Housing Watch

Subscribe to: Posts