Thursday, August 9, 2018

Housing Market in Hungary

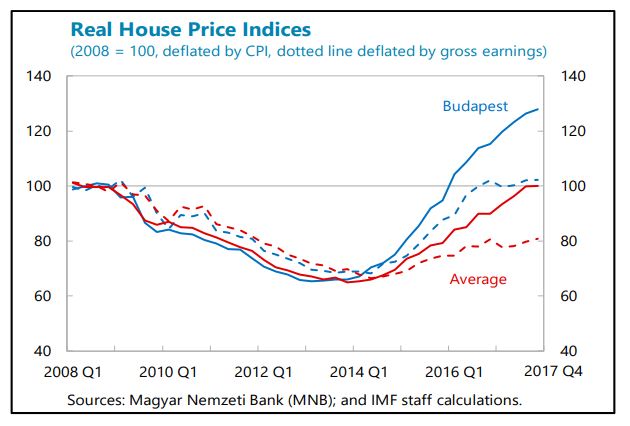

From the IMF’s latest report on Hungary:

“Hungarian housing prices have increased rapidly since 2014, but from a low level. House prices began to increase in the Budapest area, but have spread to other cities and more recently to municipalities. According to the MNB’s and European Systemic Risk Board’s (data for the latter are as of Q3 2017) estimates, average prices are not yet excessively overpriced compared to fundamentals. The number of transactions has begun to stabilize, possibly due to labor shortages and increasing construction costs, which, according to market observers, frequently delay the completion of new dwellings by 6–12 months.

The housing boom has been driven by many factors other than credit. Delayed purchases following the global financial crisis as well as fiscal initiatives have contributed to the boom. For instance, (i) young families committed to have three or more children can receive a grant and a subsidized loan to purchase a home; and (ii) the VAT rate on sales of certain new dwellings has been temporarily reduced from 27 to 5 percent during the 2016–2019 period. Moreover, low interest rates have made real estate investments more attractive. The MNB’s mortgage bond purchase program may have further supported the market. Finally, the MNB-certified consumer friendly housing loans introduced in 2017, has helped level the playing field, lowered borrowing costs, and encouraged fixed-rate lending. The stock of loans for house purchases increased by 6.8 percent (y-o-y) in May 2018. Nevertheless, according to market observers, only about 45 percent of transactions involve borrowings. Moreover, household debt in Hungary remains low compared to peers. It is also almost completely denominated in local currency, but a substantial share remains variable-rate loans.

The MNB has preventatively tightened macroprudential policies, but the booming housing market needs to be closely monitored. The various macroprudential measures seem to be working, as only about 20 percent of new lending have variable-rates or a fixed rate up to one year. Already in 2016, the calculation of the payment-to-income (PTI) ratio was changed to not discourage fixed-rate borrowing. In April 2017, the mortgage funding adequacy ratio (MFAR) was introduced to encourage banks to issue longer mortgage bonds. These ratios will be further refined to discourage interest rate risk for households in October 2018, while there are no plans thus far to change the loan-to-value ratios. However, given the fact that the boom thus far has mostly been driven by strong disposable income and fiscal incentives rather than credit and low interest rates, there is also a need to review these fiscal incentives as well as supply constraints that appear to be contributing to the boom.”

Posted by at 10:08 AM

Labels: Global Housing Watch

Subscribe to: Posts