Friday, June 15, 2018

Optimal Monetary Policy For the Masses: the James Bullard and Larry Summers View

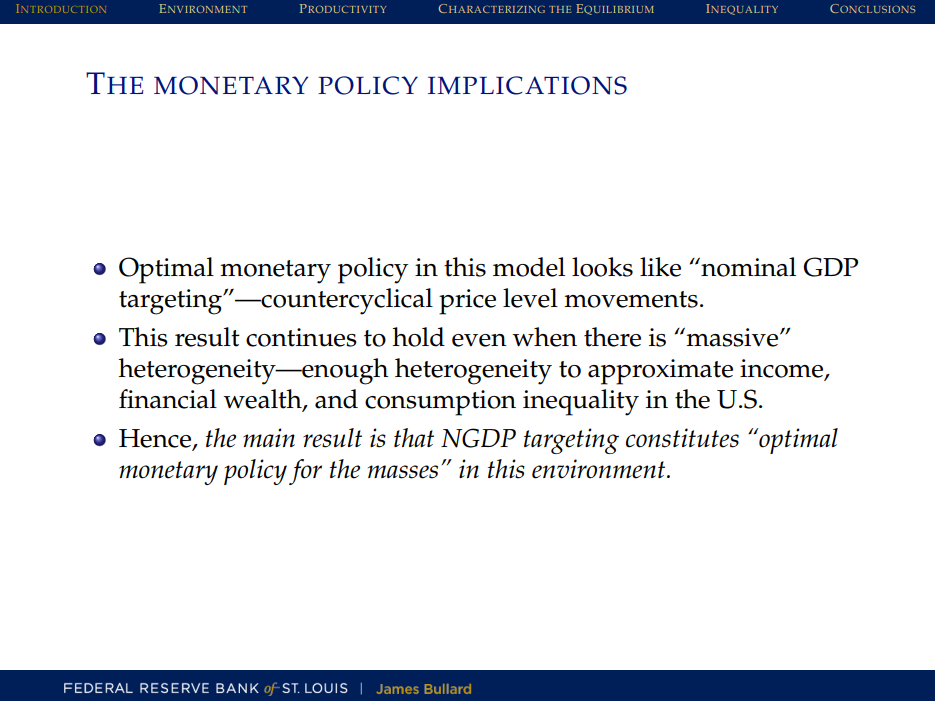

A new post by David Beckworth summarizes a new paper by James Bullard and Ricardo DiCecio:

“This paper builds upon the risk-sharing view of NGDP targeting. The basic idea is that in a world of fixed-price nominal debt contracts (i.e. the real world), a NGDP level target provides better risk sharing among creditors and debtors against economic shocks than does a price stability target.

This is because a NGDP level target makes inflation countercyclical. During recessions, inflation rises and causes creditors to bear some of the unexpected pain by lowering the real debt payments they receive from debtors. During booms, inflation falls and allows creditors to share in some of the unexpected gain by increasing the real debt payments they receive from debtors. Debtors, in other words, bear less risk during recessions but also share unexpected gains during expansions.

NGDP level targeting, in other words, causes a fixed-price nominal debt world to look and feel a lot like an equity-world. In a similar spirit, some observers have called for a risk-sharing mortgages as a way to avoid another Great Recession. The point of this paper is that the same benefit that such risk-sharing mortgages would bring can be had by having a central bank target the growth path of NGDP.”

Posted by at 10:32 AM

Labels: Inclusive Growth

Subscribe to: Posts