Thursday, June 21, 2018

Housing Market in Denmark

The IMF’s latest report on Denmark says that:

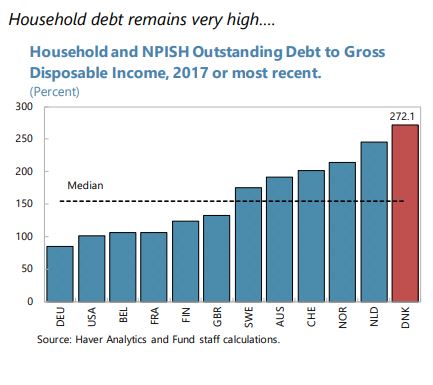

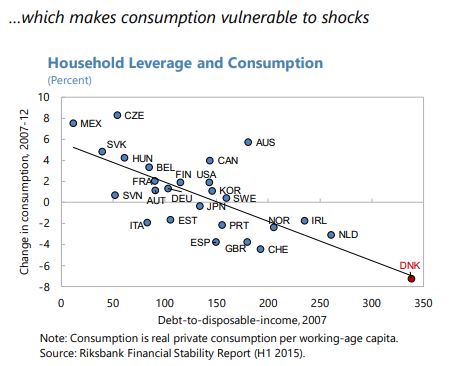

“The adverse feedback loops between housing and the real economy in Denmark are important. The centrality of housing in the Danish economy reflects at least three aspects. First, housing is a major asset of Danish households, together with pensions. Second, MCIs issue covered bonds to fund the mortgages provided to households, transferring part of mortgage risks to investors, mainly financial institutions, including pension funds and insurance companies (Figure 4). Third, because of the high real estate valuations and low interest rates, house purchases typically need to be funded via large mortgage multiples relative to disposable income. These factors help to explain why Danish households’ debt to income ratios are among the highest among advanced economies, and why consumption is sensitive to house price developments.

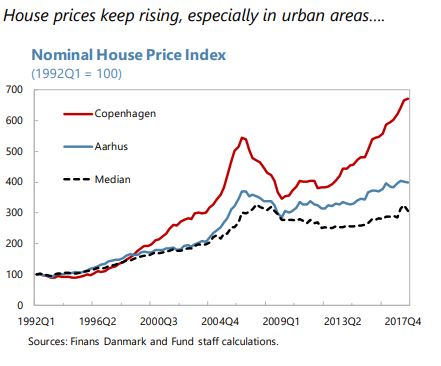

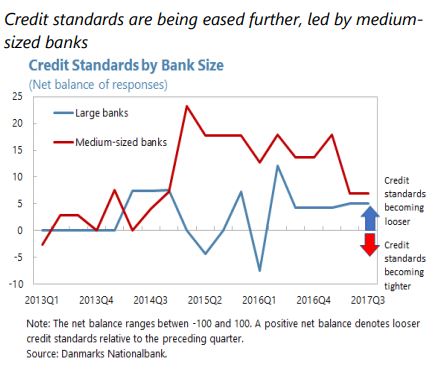

High household leverage combined with high and rising house prices could raise macrofinancial vulnerabilities. There is a risk that high and still rising house prices (particularly in urban areas), the relaxation of credit standards (Figure 4), and mortgage rates near all time-lows, may increase the perception of affordability across a broad spectrum of income levels. In this environment, two types of Danish households are particularly vulnerable to shocks. First, low-income households who spend more than 40 percent of their disposable income on housing (Figure 4). Second, households who have purchased in highly appreciating and potentially overvalued urban areas such as Copenhagen (Selected Issues), where LTI ratios and credit growth are noticeably higher than in the rest of the country. These vulnerabilities are compounded by the large proportion of variable-rate and interest-only mortgages in the system.

In recent years, authorities have implemented an extensive package of policies to address rising vulnerabilities. These include diverse macroprudential policies, 10 various supervisory guidance for MCIs and banks, and a reform of property taxation (Denmark 2017 Article IV report). The authorities continued building their macroprudential toolbox. Following the March 2017 Systemic Risk Council’s recommendation to limit lending via interest-only and floating-rate mortgages to high DTI households in areas with rapid housing prices growth, authorities introduced LTV restrictions. Effective from 2018, changes to consumer protection rules limit lending via interest-only and floating-rate mortgages to highly indebted households. Specifically, there are lending restrictions for households with DTI greater than 4 times and LTV greater than 60 percent: (i) the interest-rate fixation of floating-rate mortgages needs to be at least 5 years, and (ii) deferred amortization is only applicable on 30-year fixed-rate loans.

Coordinated policies are needed to tackle macro-financial vulnerabilities, including those stemming from excessive household leverage combined with rising house prices and affordability. Staff recognized authorities’ efforts and advocated continuing with the deployment of policies as follows.

Macroprudential instruments. The existing macroprudential measures should be tightened further. Staff analysis suggests that the LTV limit should be lowered from 95 to 90 percent to better protect households from house price declines. This decrease would lower aggregate consumption by about 1.5 percentage points one year after introduction, but increase it by 0.2 percentage points in a new steady-state because of lower debt-servicing costs (Denmark 2016 Article IV, Selected Issues). Thus, tightening the LTV limit would have a positive spillover by alleviating demand pressures in the near-term. DTI restrictions should be strengthened for all loans irrespective of LTV considerations. Tighter DTI limits for interest-only and adjustable-rate mortgages should also be considered to contain leverage, increase resilience, and limit the drag on consumption. Highly leveraged households—with debt-to-income above 400 percent—should be subject to mandatory amortization.11 To encourage further reduction of interest-rate sensitivity, the DTI limit could be calibrated to account for lower risk if financing is via fixed–rate mortgages.

Tax policy. Mortgage interest deductibility (MID) should be reduced further than currently planned, as MID distorts investment incentives and incentivizes leverage (Gruber, 2017). During the transition period to a lower mortgage deductibility regime, the current low rate environment would mitigate the adverse impact on homeowners. Also, fiscal savings from this measure could be used to reduce labor tax burden.

Housing supply. Restrictions on the size of new apartments should be relaxed in urban areas where demand-supply imbalances appear to have been a factor pushing valuations higher.

Simpler and more streamlined zoning and planning processes would allow housing supply to respond to increases in demand without steep price increases. Rent controls are among the highest in the EU and should be reduced to incentivize the rental market and alleviate demand for housing. Below-market rents limit the incentive to supply rental units, and incentivize the purchase of housing, adding upward pressure to property prices. Upgrading public and transport infrastructure—especially around inner-city areas experiencing strong house price growth—would help mitigate house prices pressures.The interaction between high household leverage and rising house prices poses macrofinancial risks. Authorities indicated that household resilience to interest rate increases likely improved as more homeowners had shifted towards fixed rate mortgages and longer fixing periods. But if risks continue to build up, the DN sees scope for tighter LTV limit, higher countercyclical capital buffer, amortization requirements and reduction of variable-rate loans. The government argued that additional measures would require further analysis of the effects on the housing market and the overall economy. The government considers unlikely that mortgage interest deductibility will be reduced beyond the planned gradual decline ending next year, and noted that mortgage interest deductibility should take into account balances towards other capital taxation rates.”

Posted by at 11:23 AM

Labels: Global Housing Watch

Subscribe to: Posts