Wednesday, June 27, 2018

House Prices in Lithuania

The IMF’s latest report on Lithuania says that:

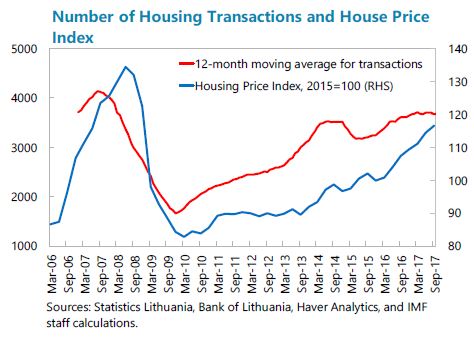

“Household credit remained strong, rising by 7 percent thanks to solid wage growth, and coincided with a surge in housing activity. The number of transactions in the real estate market rose sharply and neared the pre-crisis peak. Moreover, housing prices, especially in major urban centers, rose sharply, prompting the Bank of Lithuania (BoL) to raise the countercyclical capital buffer by 0.5 percentage points in December 2017. Nonetheless, the stock of credit is still modest at 41 percent of GDP, well below the pre-crisis peak of 68 percent of GDP. Similarly, housing prices remain significantly below their 2007 peak, especially when adjusted for inflation. Financial soundness indicators remain strong. Lithuania’s banking system is well capitalized, liquid, and profitable despite the low interest rate environment. Nevertheless, spillovers from real-estate related vulnerabilities in Nordic parent banks, which control most of Lithuania’s financial sector, remain a risk.”

The report also says:

“An analysis of Lithuania’s credit, housing price, and output cycles during 1995–2017Q3, reveals that housing price cycles are more frequent, but shorter-lived than the other two with credit cycles being the most volatile. The analysis finds strong synchronization among them in Lithuania, particularly between the credit and housing price cycles.

Lithuania’s cycles are highly synchronized with those of other Baltic and Nordic countries. This is particularly true for credit due to the close links of Lithuania’s financial system to parent bank developments. Housing price cycles are the least synchronized possibly because real estate markets are mostly affected by local conditions.

An econometric exercise shows that housing price booms are the key determinant of credit upturns. Other factors causing a credit upturn include the negative impact of the global financial crisis, bank profitability, deposit growth, interest rates, and private sector indebtedness. The presence of an economic boom does not seem to be a significant determinant of a credit upturn, suggesting that other, potentially external, factors play a more significant role.

A panel VAR that includes other variables potentially influencing credit demand and supply shows that Lithuania is more vulnerable to shocks than the region as a whole, and that credit and real GDP shocks in Lithuania have a particularly strong impact on Lithuania’s credit. Credit, housing price, and output shocks in other Baltic and Nordic countries on average also have a strong impact on Lithuania’s credit.”

Posted by at 6:56 AM

Labels: Global Housing Watch

Subscribe to: Posts