Tuesday, April 24, 2018

Understanding Singapore’s Housing Market

Global Housing Watch Newsletter: April 2018

In this interview, Sock-Yong Phang talks about her new book on Singapore’s housing market—Policy Innovations for Affordable Housing In Singapore: From Colony to Global City. Phang is Celia Moh Chair Professor of Economics at the Singapore Management University, Singapore.

On key characteristics of Singapore’s housing market…

Hites Ahir: How is Singapore’s housing market unusual compared to the housing market in other countries?

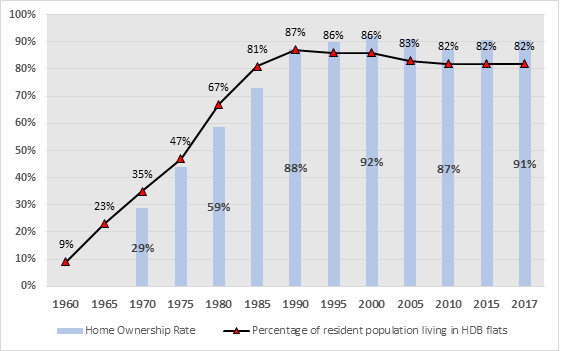

Sock-Yong Phang: Singapore has a very high homeownership rate of 91 percent, and the government’s involvement in the housing market is rather unusual. The Housing and Development Board (HDB), a statutory board of the Ministry of National Development, is the largest housing developer. In 1960, 9 percent of the population lived in rental public housing. By 1985, four-fifths of the resident population were living in HDB flats. More than 90 percent of HDB’s housing have been sold on 99-year lease tenure to eligible households – at below market prices. Buyers can sell their HDB flats in an active secondary market at market prices after 5-years.

Chart 1: Resident Population Living in HDB Flats and Homeownership Rate

Data sources: Singapore government websites

Hites Ahir: What are the key housing policies that have made a difference to Singapore’s housing market?

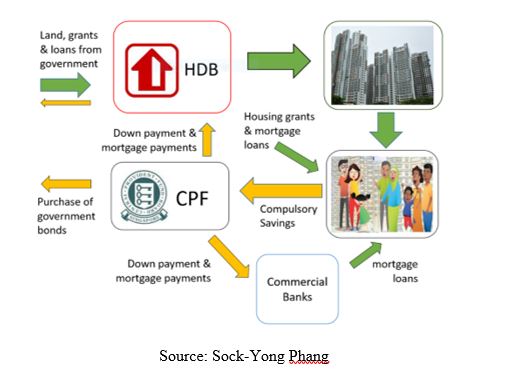

Sock-Yong Phang: One key policy is that HDB housing has transformed the physical and socioeconomic landscape. Another key policy in 1968 allowed Central Provident Fund (CPF) savings to be withdrawn by members for housing down payment, and mortgage payments. The HDB and CPF together formed an integrated sustainable framework for affordable homeownership.

Chart 2: An integrated sustainable framework for affordable homeownership

Hites Ahir: In your new book, you talk about Henry George—an American economist. Can you talk a bit about his ideas, and how it relates to Singapore?

Sock-Yong Phang: In 19th century America, Henry George observed that the explosive growth of industrial output generated dramatic increases in urban land prices. The windfalls for landowners, in turn, fueled a frenzy of land speculation and real estate bubbles and volatility. While industrialists, bankers and landowners amassed enormous wealth in the Gilded Age, there was a simultaneous rise in poverty, inequality, and social unrest. In 1879, George published a critique of the capitalist system in Progress and Poverty. His controversial view was that land should be common property, and society should share in any increase in land rents. His proposal was for a 100 percent single tax on land values.

A commentator of an article I wrote described Singapore as ‘the most Georgist” place on earth. However, there is no mention of George in the intense policy debates on land policy in the 1960s. The policymakers of that era recognized the huge importance of land to jumpstart the economy, and the housing program. Their observations on the unfairness of unearned land value increments, the negative impacts of land speculation, and the need for the state to capture land values mirrored those of George’s. However, the policies they implemented differed. These policies include compulsory state land acquisition at below market prices, development charges, and government land sales.

The state’s ownership of more than 90 percent of land enabled coordinated land use planning, and flexibility to shift allocations among competing needs for economic development. Greater reliance on land-based revenues also made feasible lower taxes on businesses, and employment. Effective land value capture facilitated growth-enhancing public-sector investments in urban infrastructure, industrial parks, urban redevelopment projects, and redistribution through HDB housing.

On affordable housing and inequality…

Hites Ahir: How does Singapore finance affordable housing for its low, and middle-income groups?

Sock-Yong Phang: Singaporeans typically purchase their first home from the HDB. The HDB provides up to 25-year mortgage loans, at an interest rate of 2.6 percent. HDB prices are below market prices, and buyers enjoy additional discounts in the form of housing grants calibrated to incomes. The government sells land to the HDB, and fully finances its annual deficit. Within the housing sector, there is a high degree of progressive taxation. Higher-income households, foreigners, and investors pay market prices, implicit higher land taxes, higher stamp duties, and are subject to higher rates of property taxes.

Hites Ahir: In the book, you also talk about housing market segmentation for housing affordability. Could you elaborate on this?

Sock-Yong Phang: If someone were to ask me for advice on what housing to buy, and how much it would cost, I would have to ask several questions. Are you a citizen, permanent resident, or foreigner? What is your household income? Are you a first-time buyer? Are you married or single? If single, how old are you? Do you plan to live near or with your parents? What is your ethnicity? These questions give a sense of the means testing, and profiling used for market segmentation. Spatially though, careful land use planning and quotas are used to integrate different household types for inclusive neighborhoods.

Hites Ahir: Did Singapore had to deal with the formation of slums?

Sock-Yong Phang: Slums and squatter settlements were prevalent in Singapore in the 1960s when a majority of the population lived in crammed conditions in pre-war shophouses, and attap/zinc-roofed housing. It was under such dire conditions that the government made improvements to housing conditions a key priority.

Hites Ahir: In the book, you also say that growing inequality has become a concern worldwide. “Discussions about solutions to tackle the challenges of poverty and inequality have tended to revolve around higher taxes on wealth and labor market interventions such as minimum wages and universal basic incomes.” What has Singapore done?

Sock-Yong Phang: Singapore has used housing policies extensively to mitigate wealth inequality. The housing tax and subsidy regime is highly progressive. Interestingly, I estimated the gross housing wealth distribution, and found it approximates the capital ownership distribution in Thomas Piketty’s vision of an ‘ideal society’.

On foreign investors and speculation…

Hites Ahir: For the past two-three years, there has been a lot of discussion on the impact of foreign investors, and speculation in the housing market. Has Singapore done anything on this? Did it work?

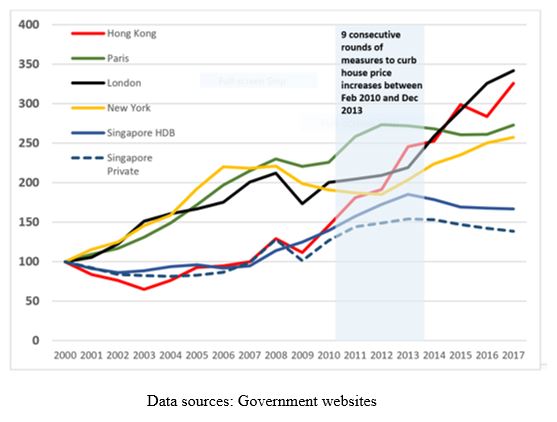

Sock-Yong Phang: Housing is an important consumption item, and household asset. Prices should not be dependent on foreign speculators and investors, foreign monetary policies, and global liquidity. Singapore keeps foreigners out of the HDB, and the landed housing sectors. Foreigners can only buy private condominiums – which are about 20 percent of the market. Despite this, price spillover effects to other protected market segments led the government to impose 9 rounds of measures to discourage foreign, and investment demand from 2010 to 2013. The instruments deployed include stamp duties, and caps on borrowing. These measures, in combination with an increase in housing supply, and slower population growth, worked – price increases started to taper off by late 2013.

Chart 3: Effectiveness of measures to curb house price increases in Singapore: comparison with house price trends (nominal prices) in 4 other global cities

On other issues…

Hites Ahir: Singapore has a homeownership rate of 90 percent. Why is the rental market not attractive or promoted?

Sock-Yong Phang: The Singapore government is, generally speaking, non-ideological, with a practical, pragmatic approach to economic policies. However, homeownership has almost the status of an ideology in Singapore. This has worked for a city-state where spatial mobility is less of an issue, and has allowed low and middle-income households to own an asset, and benefit from housing price appreciation.

Hites Ahir: Can you talk about how the median age of the population has changed over time, and what challenges this presents?

Sock-Yong Phang: The median age increased from 34.0 years in 2000 to 40.5 in 2017. Lower-income ageing homeowners are often “housing asset rich and cash poor”. The government has devised schemes to help homeowners liquidate housing equity for retirement financing. One option is to downsize to a smaller or shorter lease HDB flat. Another scheme allows homeowners to sell the tail-end of their property’s lease to the HDB. However, the low take-up rate remains a puzzle.

Hites Ahir: Why do you think it is difficult to find strong advocates for government centered housing welfare systems?

Sock-Yong Phang: Housing markets are incredibly complex. Policies designed with good intentions can go wrong, or they can become entrenched over time. Examples of policy failure include socialist housing systems, rent control, US public housing projects, and the subprime mortgages crisis. My 2013 book Housing Finance Systems: Market Failures and Government Failures has extensive discussion on these challenges.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts