Wednesday, February 14, 2018

Korea: Macroprudential Policy and High Household Debt

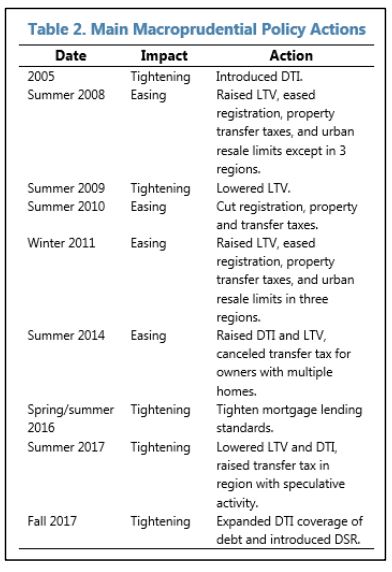

From the latest IMF’s report on Korea:

“Macroprudential policies are being extensively used to curb risks from high household debt and credit growth. A broad range of macroprudential instruments that have been tightened and new ones introduced (Table 2). The loan-to-value (LTV) and debt-to-income (DTI) ratios were reduced to record lows of 40 percent, and are now well below recent highs of 70 and 60 percent, respectively, to which they were increased in August 2014. And, a lower level of 30 percent was set for borrowers with multiple mortgages and in designated regions of speculative activity, mostly around Seoul. In October 2017, the DTI was effectively tightened further by broadening the range of debt subject to it. Also announced is a new, debt service ratio (DSR) with comprehensive coverage of all household debts, which will be implemented for banks in mid-2018; and then for NBFIs at the start of 2019.

Evidence suggests that this macroprudential tightening will be effective. The growth in credit to households has slowed significantly over the last few months. Moreover, speculative purchases of apartments before construction is has diminished. An event study analysis by Federal Reserve Board economists finds that hikes in LTVs and DTIs have been effective in slowing credit growth and housing price increases. New cross-country panel regression analysis show that use of LTVs and DTIs is effective in reducing real household credit growth across 34 advanced and emerging market economies, including Korea.”

Posted by at 9:55 AM

Labels: Global Housing Watch

Subscribe to: Posts