Thursday, June 15, 2017

Rodrik on Financial Globalization and Inequality

Dani Rodrik writes:

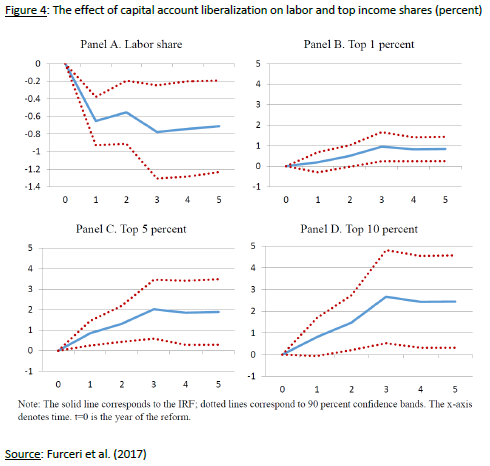

“Financial globalization appears to have produced adverse distributional impacts within countries as well, in part through its effect on incidence and severity of financial crises. In a remarkable series of papers, researchers at the IMF have documented these negative inequality impacts (Jaumotte et al. 2013; Furceri and Loungani 2015). Most noteworthy is the recent analysis by Furceri et al. (2017) that looks at 224 episodes of capital account liberalization, most of them taking place during the last couple of decades. Liberalization episodes are identified by big changes in a standard measure of financial openness (the Chinn-Ito index) and large subsequent capital flows. They find that capital-account liberalization leads to statistically significant and long-lasting declines in the labor share of income and corresponding increases in the Gini coefficient of income inequality and in the shares of top 1, 5, and 10 percent of income (see Figure 4 for their key results). Furthermore, these adverse effects on inequality are stronger in cases where de jure liberalization was accompanied by large increase in capital flows. Financial globalization appears to have complemented trade in exerting downwards pressure on the labor share of income.

Why would financial globalization increase inequality and the capital share in particular? There is no analogue to trade theory’s Stolper-Samuelson theorem in international macroeconomics. So to some extent these distributional consequences of financial globalization are a genuine surprise. But there may be an obvious, bargaining-related explanation (as argued in Rodrik 1997, chap. 2). As long as wages are determined in part by bargaining between employees and employers, the outside options of each party play an important role. Capital mobility gives employers a credible threat: accept lower wages, or else we move abroad. Indeed, Furceri et al. (2017) provide some evidence that the decline in the labor share is related to the threat of relocating production abroad. As a proxy for the potential threat they use layoff propensities of different industries. They find the effect of capital account liberalization on labor shares is particularly strong in those sectors with a higher natural layoff rate. The bargaining explanation is also consistent with the finding in Jaumotte et al. (2013) that it is foreign direct investment in particular that is associated with the rise in inequality.”

Continue reading here.

Posted by at 9:11 AM

Labels: Inclusive Growth

Subscribe to: Posts