Friday, February 10, 2017

House Prices in Australia

The IMF’s annual report on Australia points out that:

“By some metrics, housing market conditions have cooled and credit growth to households has slowed, but risks related to house price and debt levels have not yet decreased.

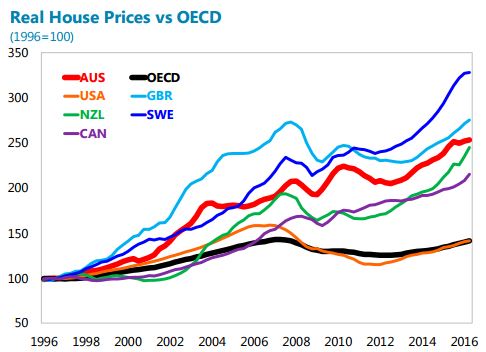

Real house price gains have moderated. Indicators of current conditions such as sales volumes and the rate of turnover in the housing stock have moderated. The extent of cooling has varied considerably across capital cities. The strongest price increases continue to be recorded in Sydney and Melbourne, where underlying demand for housing remains strong. With house prices still rising ahead of income, standard valuation metrics suggest somewhat higher house price overvaluation relative to the assessment in 2015 Article IV consultation.

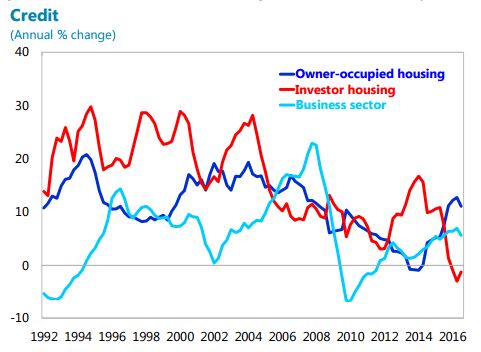

The flipside has been slowing growth in bank lending to households. APRA prudential guidance requiring tighter lending standards by banks, which was introduced in late 2014, has curtailed growth in riskier mortgage loans in particular and credit growth to household more broadly. At the same time, there has been some upward pressures on mortgage rates, as banks have increased capital ratios and prepared for a higher risk weight on mortgage lending. That said, household credit gaps have not yet reversed.

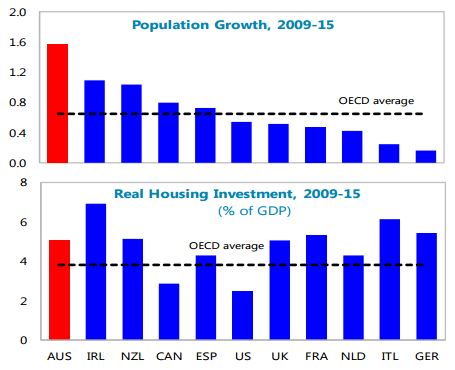

On the supply side, residential investment has risen to some 0.5 percent of GDP above its long term average (the ratio remains comparatively low given population and labor force growth). An above-average number of new apartments is expected to come on stream in the next year or so, mostly in the downtown areas of Brisbane, Melbourne, and, to a lesser extent, Sydney. Concerns about temporary oversupply have thus risen. But leading indicators, such as approvals of new houses and other dwellings or new residential construction starts, have started to level off after brisk increases in 2014-15. In commercial real estate, property price valuations have increased but are still within the usual range of variation over the cycle (..).“

Posted by at 12:46 PM

Labels: Global Housing Watch

Subscribe to: Posts