Wednesday, January 27, 2016

Four Questions About Recent Developments in UK’s Housing Market

Please bear in mind that this is intended to be a summary of views of external analysts and should not be attributed to the IMF.

“12 months of growing crisis”—that’s how the Guardian summarizes the housing market developments of 2015. This could partly explain the recent housing market measures announced by the UK government. However, experts doubt that these measures will have any effect. What follows is an attempt to answer four key questions about these developments:

- What are the new policies that the UK government announced?

- Will house price head north or south?

- What can be done?

- What are the likely implications?

1. What are the new policies that the UK government announced?The short answer: a series of measures to ease house prices and boost the housing supply.

2. Will house prices head north or south?

The short answer: north.

The long answer: “Government initiatives to support home ownership and build new houses will fail to have any real impact in 2016, with UK property prices expected to keep climbing”, according to a recent Financial Times survey. The survey asked 88 economists the following question: What effect are government policies likely to have on the housing supply and demand in 2016? How much will they contribute to likely changes in house prices?

The result of the survey is consistent with other data showing a similar upward trend in house prices. According to another survey, there is a pick-up in both activity and price expectations reflecting a rush to purchase Buy To Let properties ahead of the change in the Stamp Duty in April, according to Simon Rubinsohn at Royal Institution of Chartered Surveyors. Moreover, “The housing market has enjoyed some smooth sailing in the past year, with a steady 6.6% growth in house prices during 2015 (…) If the current speed of house price growth continues into 2016, the value of the average home may soon pass the £300,000 watermark, having reached £250,000 in December 2013”, according to LSL Property Services/Acadata. The latest numbers from Halifax, Knight Frank, and Office for National Statistics also points to an upward trend in house prices.

The short answer: it is complicated.

The long answer: on one hand, there seems to be a consensus among the experts that rising house prices is a concern and that there is not enough housing supply. On the other hand, there doesn’t seem to be any consensus on what the best way is to deal with rising house prices and expanding the supply of housing.

For example, experts have different views on how to address the housing supply problem. Martin Wolf of the Financial Times proposes that “The government must slay the sacred cows — the greenbelts around cities being the holiest of all.” In contrast, “Building an extra 100,000 houses a year would make hardly any difference to the upward trajectory of prices,” according to Gordon Gemmill of the University of Warwick. Oliver Jones of Fathom Consulting says: “(…) the problem in the UK is not a shortage of supply, but an excess of demand (…)”. The Economist says: “Building more houses is only part of the remedy for high prices (…) For one thing, Britain is bad at putting houses where they are most needed.” Melanie Baker and Jacob Nell of Morgan Stanley say that “There are so many government policies on housing that it is difficult to be confident about the net impact.”

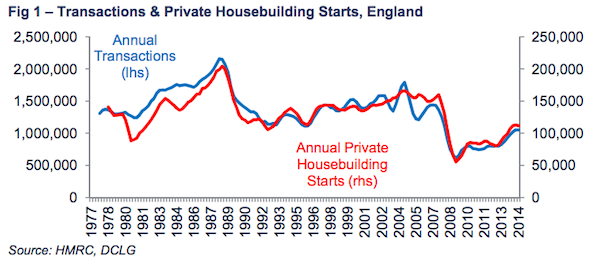

The complexity of the housing supply debate can also be seen in the chart above. It comes from Neal Hudson, of Savills, and reveals a bizarre relationship. It says: “This chart has big implications. Everyone goes on about how Britain needs to build 250,000 or so houses each year to keep up with demand. The chart, of course, implies that unless you get housing transactions up, private builders won’t get anywhere near that figure (the public sector build very little housing). Now, the big question is: why does this relationship exist? Economists don’t really know. However, here is one suggestion (…) Housebuilders, (…) tend to target the price of new-build houses at the upper decile of the prices prevailing in the local property market (ie, at the top 10% of all the houses sold nearby in a given period of time). If that is true, then you would expect there (roughly) to be one house built for every ten sold.”

4. What are the likely implications?

The short answer: among other things, rising house prices will likely lead to bigger mortgages and more affordability problems.

The long answer: Mortgages that extend over 35 years are now quite normal and may even overtake the traditional terms of 20-25 years (Halifax). “All else being equal, it’s an odd trend. Interest rates remain at record lows so it should be easier to afford a shorter tenure for your borrowing”, says Patrick Jenkins of the Financial Times. “But of course all else is not equal. The cost of the average home jumped again last year by more than 6 per cent, and in London by more than 11 per cent. To cope, home buyers are borrowing higher sums over longer periods. For the same monthly repayment, you can fund a 20 per cent bigger mortgage if you borrow over 35 years instead of 25”, according to Jenkins. In 2014, Andrew Bailey of the Bank of England pointed out that if mortgages extend into retirement when incomes fall “we have a long-term problem”.

Moreover, “property is set to become even more unaffordable going forward”, says Simon Rubinsohn at Royal Institution of Chartered Surveyors. “So building more houses is the key to solving the problem, right? — Well, not exactly. It only works if house builders build a glut of homes that people can afford”, notes Lianna Brinded at Business Insider. More recently, UK ministers have been criticized for broadening the definition of affordable housing. The new definition “(…) includes so-called starter homes costing up to £450,000 — 17 times the average British salary” (Financial Times). Meanwhile, Politico says that what “(…) should worry those in Brussels who desperately want the U.K. to stay part of the EU is its housing market. (…) In broad terms, there is a shortage of good quality affordable housing, particularly in the southern half of England.” Finally, the New Economic Foundation takes a look at the human cost of the housing crisis.

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts