Wednesday, December 23, 2015

Understanding China’s Housing Market

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”, in 2013. “End of the golden era: China’s property market is cooling off, at long last”, in 2014. These days, together with the housing market, analysts are also expressing concerns about the overall health of the Chinese economy. Here is one headline from 2015: “Coming down to earth: Chinese growth is losing altitude. Will it be a soft or hard landing?”

So why China’s housing market has not seen a bust yet? At last weekend’s conference in Shenzhen on December 18-19, leading experts on China’s housing market provided some answers. The conference—International Symposium on Housing and Financial Stability in China—was organized by the Chinese University of Hong Kong in Shenzhen, International Monetary Fund, and Princeton University.

Getting the facts right: housing and mortgage market

New research by Joe Gyourko (University of Pennsylvania) and his co-authors provides facts on China’s housing market from a supply and demand perspective. “In China, different housing markets behave very differently. A boom in Beijing and Shenzhen doesn’t mean a boom everywhere”, Gyourko said at the conference.

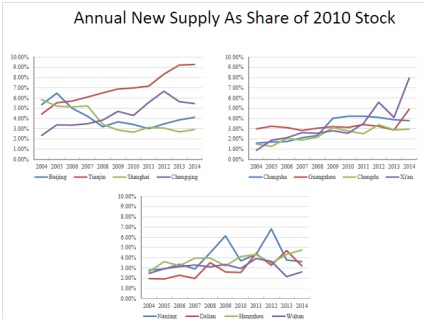

In his presentation, Gyourko made two key points. First point: there is substantial heterogeneity across cities in the balance between housing supply and demand. At one end, housing supply has outpaced demand in the interior part of the country. Specifically, housing supply has outpaced demand by at least 30 percent in twelve major markets and by 10 to 29 percent in another eight markets. On the other end, housing demand has outpaced supply in most major eastern markets. These include: Beijing, Hangzhou, Shanghai, and Shenzhen. Second point: markets such as Beijing, despite their strong measured fundamentals, should be considered somewhat risky because homes there trade at very high multiples of rent.

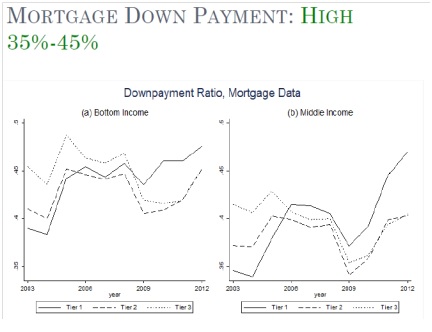

Another new piece of research, by Hanming Fang (University of Pennsylvania) and his co-authors, provides facts on China’s housing market from the mortgage market perspective. They have constructed a set of house price indices for 120 major cities in China and used a comprehensive data set of mortgage loans from 2003 to 2013. In his presentation, Fang showed that the Chinese housing boom has been accompanied by strong growth in income, and high mortgage down payments. For a decade, household’s disposable income has had an average annual real growth of 9 percent at the national level. Also, down payments have been over 30 percent on all mortgage loans.

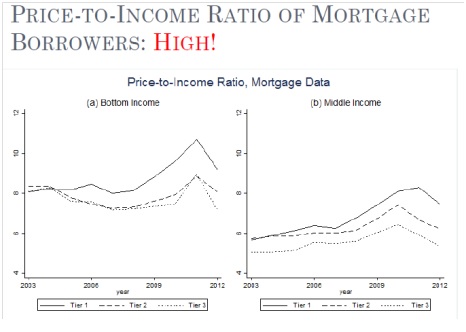

However, Fang noted that the participation of low-income home buyers in the housing boom has been characterized by high price-to-income ratios. The ratios are around eight in second and third tier cities, and even ten in first tier cities.

Haizhou Huang (CICC) provided very interesting facts on China’s housing market from the perspective of population in big cities. Huang pointed out that population concentrates into big cities. For example, in Japan and the United States, an increase in urbanization was accompanied by an increase in population concentration in big cities. So Huang expects that population concentration in China’s big cities will continue to rise. This could lead to more pressure on the housing market in Tier 1 cities. Huang asks: “Should China follow the European or Japanese model of few cities that have a large amount of the population?” China needs to develop more megacities, in his view. This could imply that the housing market could continue to grow and pressure in the housing market in tier I cities could decrease in the future.

Xiaobo Zhang (Peking University) talked the impact on China’s housing market from cultural traditions. “In rural areas of China, a new home is a necessary condition for marriage”, says Zhang. This is due in part by the sex ratio imbalance in China. Zhang showed that in 2000, 1 in 14 males could not marry. And in 2005, it was 1 in 10.

Assessing the risks: the role of expectations and local government debt

One area of risk is the role of expectations. Fang and Gyourko said that risks in Chinese housing market could arise with a shift in expectations. Specifically, Fang said that the willingness of low-income homebuyers to endure high price-to-income rations is explained by expectation of continued growth in income. However, the high expectation of future income growth may not be sustainable. Likewise, Gyourko said that a modest downward shift in expectations could generate sharp decline in house prices.

Moreover, Richard Koss (Global Housing Watch Initiative) compared how expectations have played an important role in the housing market in China and the United States. In both countries, expectations have played a role, but in different ways. Koss said that in the United States, expectations played a role in terms of house prices (e.g. expectations that house prices would continue rising), while in China, expectations play a role in terms of income growth (e.g. expectations that income will continue rising).

In the United States, said Koss, “No one thought house prices could fall as they never had on a nationwide basis, although specific regions suffered declines in the past. Americans thought they were special and that financial innovation would minimize risks but that turned out to be completely wrong.” So, in China, there could be risks in terms of irrational expectations of income growth.

Another area of risk is the local government debt and its linkage with the housing market. A new paper by Yongheng Deng (National University of Singapore) and his co-authors explores this link. At the conference, Deng noted that unlike local governments in western countries, local Chinese governments are prevented from directly issuing debt to fund mandated capital projects. Therefore, local governments tap into the growing housing market by selling public land to rise funding.

More specifically, future land sales revenue are used to repay the local government’s debt and land parcels are the most widely-used collateral for local government debt. This implies that “a substantial drop in housing or land prices may increase the risk level of local government debt, or even trigger a systematic default”, said Deng.

Posted by at 4:46 PM

Labels: Global Housing Watch

Subscribe to: Posts