Thursday, October 1, 2015

Are Australia’s House Prices Overvalued?

Below is the argument, counter arguments, and the bottom line from the study:

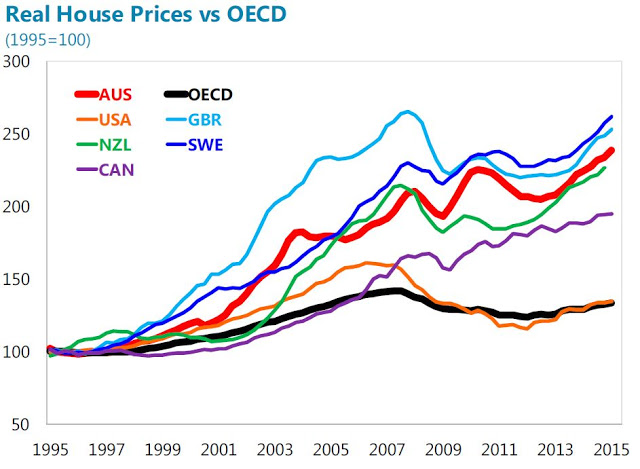

Argument: House prices have risen faster in Australia than in most other countries, suggesting, ceteris paribus, overvaluation

Counter argument 1: House prices are in line on an absolute basis

Bottom line: Price-to-income ratios have risen across all measures in Australia and are now near historic highs. However, international comparisons of price-to-income ratios suggest that Australia is broadly in line with comparator countries, although significant data comparability issues make inference difficult.

Counter argument 2: The equilibrium level of house prices has also risen sharply

Bottom line: Lower nominal and real interest rates and financial liberalization are key contributors to the strong increases in house prices over the past two decades. The various house price modeling approaches indicate that house prices are moderately stronger (in the range of 4-19 percent) than economic fundamentals would suggest.

Counter argument 3: High prices reflect low supply

Bottom line: housing supply does indeed seem to have grown significantly slower than demand, reducing (but not eliminating) concerns about overvaluation.

Counter argument 4: It is just a Sydney problem, not a national one

Bottom line: The two most populous cities, Sydney and Melbourne, have seen strong house price increase in recent years, including in the investor segment. A sharp downturn in the housing market in these cities could be expected to have real sector spillovers, pointing to the need for targeted measures –including investor lending-to reduce the risks related to a housing downturn.

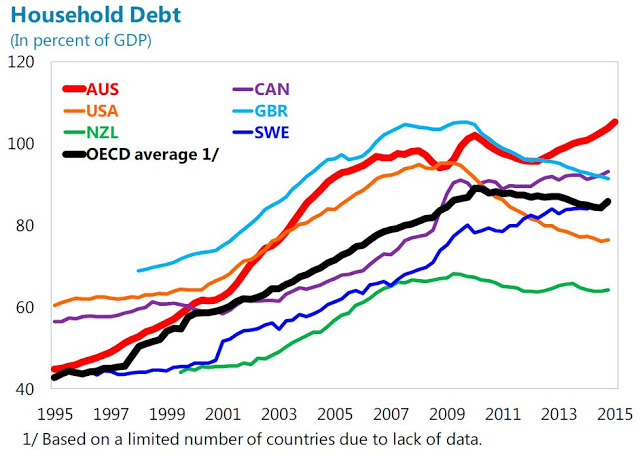

Counter argument 5: There are no signs of weakening lending standards or speculation

Bottom line: While lending standards overall seem not to have loosened, the growing share of investor and interest only loans focused on the highly-buoyant Sydney market, is a pocket of concern.

Counter argument 6: Even if they are overvalued, it doesn’t matter as banks can withstand a big fall

Bottom line: While bank capital levels are likely sufficient to keep them solvent in the event of a major fall in house prices, they are not enough to prevent banks making an already extremely difficult macroeconomic situation worse.

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts