Monday, September 14, 2015

Metals and Oil: A Tale of Two Commodities

“It was the best of times, it was the worst of times.” With these words Charles Dickens opens his novel “A Tale of Two Cities”. Winners and losers in a “tale of two commodities” may one day look back with similar reflections, as prices of metals and oil have seen some seismic shifts in recent weeks, months and years.

This blog seeks to explain how demand — but also supply and financial market conditions — are affecting metals prices. We will show some contrast with oil, where supply is the major factor. Stay tuned for a deeper analysis of the trends in a special commodities feature, which will be included in next month’s World Economic Outlook.

Metals matter

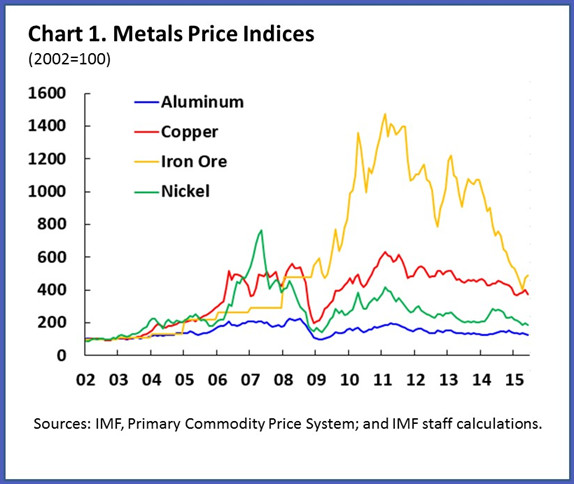

Base metals — such as iron ore, copper, aluminum and nickel — are the lifeblood of global industrial production and construction. Shaped by shifts in supply and demand, they are a valuable weathervane of change in the world economy.

There is no doubt about the direction of the prevailing wind for metals in recent years. Prices have been gradually declining since 2011 (chart 1). While oil prices have also dropped, the decline is more recent (prices peaked in 2014), and more abrupt. That said, in both cases the downward pressure on prices result broadly from abundant production from the era of high prices. This is now coming to roost with lower demand from both emerging markets and advanced economies. There are importance nuances however in the relative strength and nature of those forces.

Appetite for production

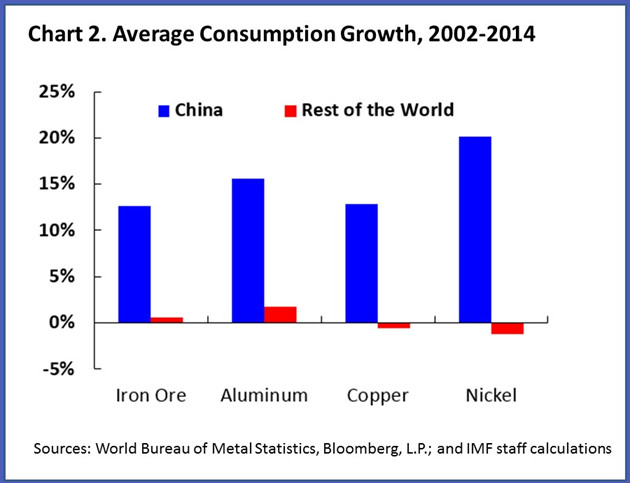

In the early 2000s, demand for metals shifted from advanced economies in the West to emerging markets in the East. China, by far the main driving force, now accounts for half of global base metal consumption (chart 2). Compare that with China’s more modest consumption of 14% of the world’s oil which is almost exclusively used for transportation.

It is therefore no surprise that metals prices are heavily influenced by demand, and the needs of one economic giant in particular. India, Russia and South Korea have also increased their metal consumption, but remain far behind China. The slower pace of investment in China in the last few years, however, compounded by concerns over future demand amid the sharp stock market decline and currency devaluation this summer, have been exerting downward pressure on metal prices.

Oil supply glut

Oil prices tell a different tale. Our view is that supply factors are playing a bigger role than demand. See also our blog from last December. OPEC’s decision to maintain its level of production and strong shale oil production in the United States — in addition to the large production capacity from earlier investment — have contributed to an unprecedented supply glut.

Posted by at 5:31 PM

Labels: Energy & Climate Change

Subscribe to: Posts