Monday, August 17, 2015

China: How Big Is the Risk of a Real Estate Slowdown and Does It Matter?

How big is the risk of a real estate slowdown? The report says:

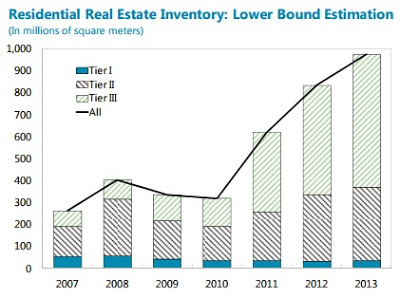

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013, suggesting oversupply. Even though there is uncertainty regarding the level (National Bureau of Statistics (NBS) data show inventory of four months, while data from local housing bureaus suggest higher than two years), the direction of the buildup is clear. Inventory is especially high in Tier 3 and Tier 4 cities.”

Does it matter? The report says:

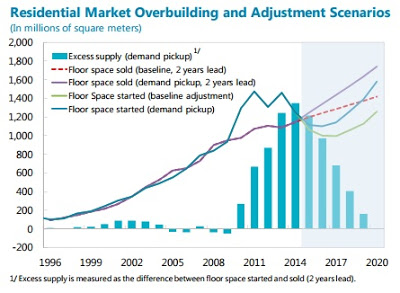

“Continued adjustment in floor space starts is warranted to let demand catch up with supply. (…) The adjustment will have significant impact on GDP growth. Given the estimated relationship between growth in floor space starts and in real estate gross fixed capital formation (GFCF), real estate GFCF could slow to -2 to -4 percent in 2015 from about 3 percent in 2014. As real estate GFCF accounts for about 9 percent of GDP, this would imply a drop of GDP growth by about ½ percentage point in the baseline scenario. This abstracts from the indirect effect arising from real estate linkages to upstream and downstream sectors. Some of these sectors suffer from oversupply, and a slowdown in construction activity could bring losses, exposing vulnerabilities and posing risks (…).”

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts