Monday, July 27, 2015

US Housing Market: An Update

Mortgage, fed funds rate, and access to credit. If you are thinking about taking out a mortgage, don’t obsess over the Fed—that’s the advice of Neil Irwin of the New York Times. Irwin says: “(…) even the most knowledgeable people about Fed policy get it wrong. I know of a guy whose insights into the Fed are better than almost anybody else’s. He refinanced his mortgage on a house in Washington in 2011, getting a 30-year fixed-rate mortgage at 4.25 percent. He should have waited a year. By late 2012, average rates were almost a full percentage point lower. But by then Ben Bernanke was stuck with his higher mortgage rate, and, presumably, a bit of regret.” On a separate note, Robert Shiller reminds us that the housing still isn’t rational (New York Times). On fed funds rate, in a recent remarks, Federal Reserve Chairwoman Janet Yellen signaled that the Fed is likely to raise its policy rate this year, assuming its forecasts for stronger growth and lower unemployment are realized. In contrast, an IMF report says that the Fed should delay policy rate rise until 2016. And on access to credit, the Urban Institute points out that access to credit is slowly increasing after years of post-crisis restriction.

Housing finance. “While a number of important steps have been taken to address the structural weaknesses exposed by the crisis in mortgage markets, comprehensive housing finance reform remains the largest piece of unfinished business. In particular, it is not clear when Fannie Mae and Freddie Mac will exit conservatorship and what an end point for a reformed housing finance system will look like. This creates not only fiscal but also financial risks: moral hazard from coverage of credit losses by the government or the government-sponsored enterprises, a distorted competitive landscape due to the dominant footprint of Fannie Mae and Freddie Mac, and large subsidies for homeownership that create incentives to take on excessive levels of household debt,” according to Deniz Igan of the IMF.

Housing market activity. On the demand front, Redfin’s new Housing Demand Index rose 13 percent in June compared to last year. Currently, the national breakeven horizon on a typical home for buyers making the median income is a little less than two years, according to Zillow. On the supply front, there is a general consensus that housing supply is tight. Bidding wars are making a comeback in a number of metro areas across the US due to a market short of homes for sale, notes the Wall Street Journal. Moreover, the lack of supply varies across the different segments. An acute lack of construction at the lower end of the housing market is creating a tight supply, driving up rents and pushing up prices of affordable homes to levels reached in 2006, says the Financial Times. On the sentiment front, home builders recently reported their highest level of satisfaction with the real estate market since 2005 (NAHB).

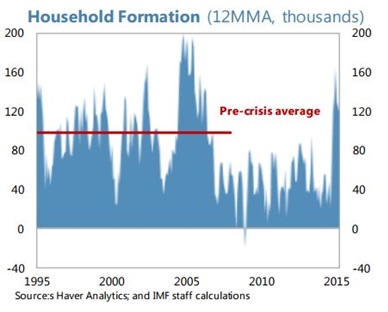

A new long-term housing equilibrium. According to an IMF report: “Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. If true, this would permanently lower the steady state growth contribution from residential construction. A less concerning interpretation comes from household surveys, which suggest that attitudes to home ownership haven’t changed much: most renters would prefer to own if they had the necessary financial resources. If that were true, once the job market improves further and millennials have paid off some of their student loans (which have grown to over US$1 trillion or 7½ percent of GDP), the demand for housing could quickly revert to previous norms, with an accompanying step-up in residential investment.”

A new long-term housing equilibrium. According to an IMF report: “Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. If true, this would permanently lower the steady state growth contribution from residential construction. A less concerning interpretation comes from household surveys, which suggest that attitudes to home ownership haven’t changed much: most renters would prefer to own if they had the necessary financial resources. If that were true, once the job market improves further and millennials have paid off some of their student loans (which have grown to over US$1 trillion or 7½ percent of GDP), the demand for housing could quickly revert to previous norms, with an accompanying step-up in residential investment.”

Rental market. The single-family rental market has enjoyed a strong run due to the foreclosure crisis and declining homeownership, according to Mark Zandi and Adam Kamins (both at Moody’s Analytics). In the long run, the rental market is also likely to remain strong. While the millennial generation born after 1980 has driven demand for apartments in recent years, baby boomers — those born from 1946 to 1964 — will be the next wave, pushing up rents and spurring construction of more multifamily housing, according to Jordan Rappaport (Federal Reserve Bank of Kansas City). There is also anecdotal evidence that developers are building few new units as demand is hit by post-crisis rules on condo mortgages (Wall Street Journal).

Debate on the causes of the recent housing crash continues. New research has focused on the reported income for mortgage loans (income reported in mortgage applications vs. income reported on tax returns). A second study from Manuel Adelino, Antoinette Schoar, and Felipe Severino finds that the results in the first study are not driven by fraudulent income overstatement as argued by Mian and Sufi. Adelino, Schoar, and Severino’s new paper show that there was no decoupling of mortgage growth from income growth at origination over the 2002 to 2006 period. Instead, their results document that mortgage debt at origination grew proportionally across the income distribution, and especially middle- and high-income and borrowers with a FICO score above 660 represented a larger share of defaults once the crisis hit. These results are hard to reconcile with the earlier view of the crisis that unprecedented levels of lending to low income and low credit score neighborhoods set off the crisis.

Posted by at 9:53 AM

Labels: Global Housing Watch

Subscribe to: Posts