Wednesday, June 10, 2015

Housing Finance and Real-Estate Booms: A Cross-Country Perspective

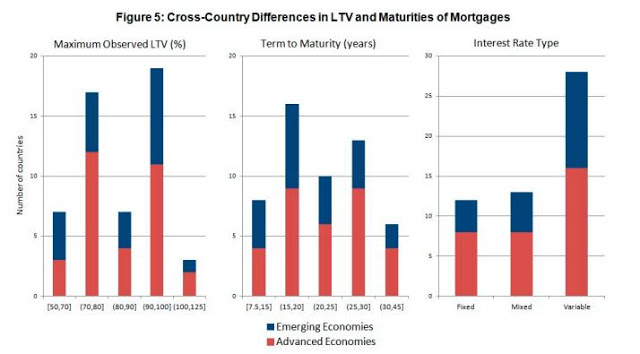

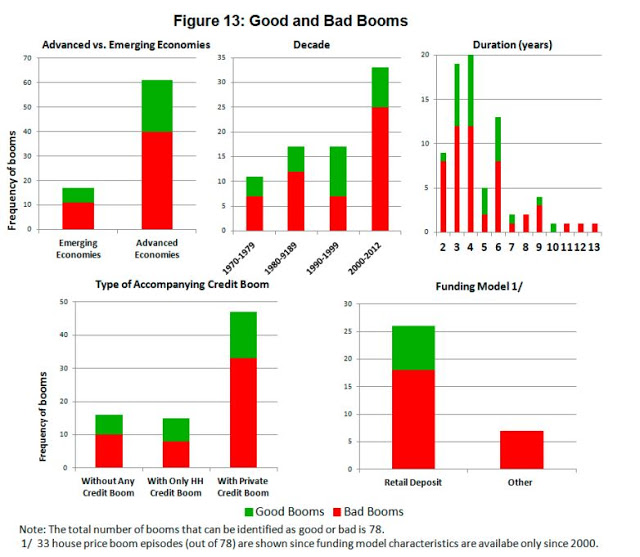

A new IMF paper “analyzes the conflict between the objective of increasing access to housing finance and the dangers associated with fast-growing housing credit. [The paper finds the following:] First, housing finance characteristics vary widely across countries, and several characteristics are correlated with the relative depth of mortgage markets. (…) Second, some of the housing finance characteristics associated with deeper mortgage markets are also associated with increased risks of crisis. (…) Third, in this context, both advanced and emerging markets should avoid relaxing house financing standards in order to achieve deeper mortgage markets, and focus first on doing so through improving institutions (for example, legal rights) and the macroeconomic environment. Fourth, macroprudential policies, and in particular housing finance regulation, should be the first line of defense for handling mortgage market booms, as their narrow focus gives them an advantage over monetary policy. However, their effectiveness beyond the short run has yet to be proven. Fifth, the role of monetary policy in addressing house-related credit booms should not always be downplayed. Despite the absence of important inflation pressures, about 60 percent of the identified past real-estate booms occurred as a result of, or at the same time as, rapid economic growth and broad high credit growth in the economy. Monetary policy would be a necessary complement of macroprudential measures in those cases. Finally, dealing effectively with real-estate booms requires a broad mix of policies. Macroprudential and monetary policies are key ingredients, but fiscal incentives and house supply considerations are structural country-specific elements that may bear heavily on the probability of booms occurring and the potential costs of a bust.”

Posted by at 5:43 PM

Labels: Global Housing Watch

Subscribe to: Posts