Wednesday, May 15, 2013

Krugman on “How the Case for Austerity Has Crumbled”

An Excerpt from Krugman’s review in The New York Review of Books

“Neil Irwin’s The Alchemists gives us a time and a place at which the major advanced countries abruptly pivoted from stimulus to austerity. The time was early February 2010; the place, somewhat bizarrely, was the remote Canadian Arctic settlement of Iqaluit, where the Group of Seven finance ministers held one of their regularly scheduled summits. Sometimes (often) such summits are little more than ceremonial occasions, and there was plenty of ceremony at this one too, including raw seal meat served at the last dinner (the foreign visitors all declined). But this time something substantive happened. “In the isolation of the Canadian wilderness,” Irwin writes, “the leaders of the world economy collectively agreed that their great challenge had shifted. The economy seemed to be healing; it was time for them to turn their attention away from boosting growth. No more stimulus.””

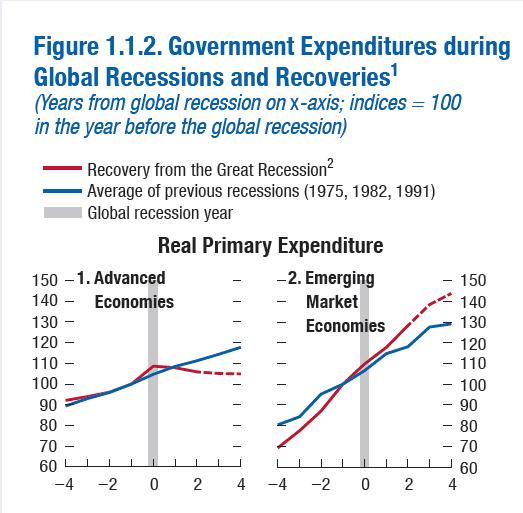

“How decisive was the turn in policy? Figure 1 [see below. Also, read the graph’s corresponding article: The Great Divergence of Policies], which is taken from the IMF’s most recent World Economic Outlook, shows how real government spending behaved in this crisis compared with previous recessions; in the figure, year zero is the year before global recession (2007 in the current slump), and spending is compared with its level in that base year. What you see is that the widespread belief that we are experiencing runaway government spending is false—on the contrary, after a brief surge in 2009, government spending began falling in both Europe and the United States, and is now well below its normal trend. The turn to austerity was very real, and quite large.”

The Great Divergence of Policies article has also been featured in the Great Recession and Not-So-Great Recovery by the Financial Times, Free to Spend, Developing Economies Recover Quicker by the New York Times, The Non-Secret of Our Non-Success by The Conscience of a Liberal Blog, and How the IMF became the friend who wants us to work less and drink more by the Washington Post.

Posted by at 7:57 PM

Labels: Forecasting Forum

Subscribe to: Posts