Sunday, April 21, 2013

Great Recession and Not-So-Great Recovery

From the Financial Times:

This week’s IMF meetings in Washington lacked the sense of crisis which has characterised many such meetings since the crash in 2008. Although the official IMF growth forecasts were revised down slightly for 2013, mainly due to tighter fiscal policy in the US, the organisation also said that downside risks, relative to the central forecasts, had diminished since the October 2012 meetings.

These improved downside risks seem to have stemmed mainly from greater confidence in the financial system, reflecting the budget deal on the US fiscal cliff, and the actions of the ECB to reduce systemic threats to the euro. Global equity markets agree with this: they are up by 13 per cent since last autumn.

There is, however, a dangerous schism between the improvements in financial confidence and the marked lack of improvement in global GDP growth. On this latter problem, the Washington meetings were focused mainly on the weakness of the eurozone, with Christine Lagarde calling for “more investment” in Germany, greater steps towards banking union and bank recapitalisation, and ECB measures to deal with fragmentation in monetary conditions between the core and the periphery. The G20 statement refrained from setting any targets for public debt reduction, which suggests that Keynesian thinking is gaining ground in international policy circles.

The IMF and the US administration are as one on all this, but my impression is (confirmed here by Chris Giles) is that the gap between Washington and Berlin is wider than ever, especially on fiscal stimulus in Germany. There is a marked sense of frustration, but also of resignation, in Washington about the German approach. Plus ça change.

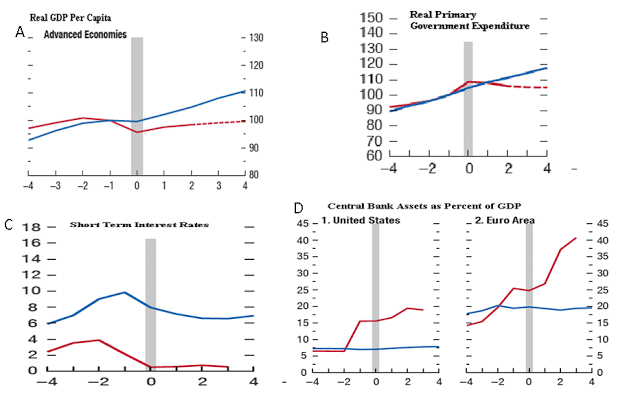

Abstracting from the details of policy in the coming months, it is important not to lose sight of the big picture for the world economy. This was well summarised in a special study on “The Great Divergence of Policies” in Chapter 1 of the IMF’s latestWorld Economic Outlook. Occasionally, a few simple graphs tell an important story:

In the graphs, the red lines represent the current cycle in the advanced economies, the blue lines represent the average of three earlier recessions (1975, 1982 and 1991), and the index numbers are centred on the year before the recessions started. An abnormally deep recession in 2008/09 has been followed by an abnormally weak recovery, so real GDP per capita is now 10 per cent below the levels indicated by previous cycles (Panel A).

Fiscal policy has been tightened everywhere to control public debt, which is much higher than “normal”, so real public spending is about 14 per cent below the cyclical norm (B). With fiscal policy tightening, the whole burden of supporting demand has fallen on monetary policy, so nominal interest rates have fallen to zero (C) and the central banks have resorted to sizeable increases in their balance sheets (D).

Questions About the Not-So-Great Recovery

This familiar story about the dramatic change in the global fiscal/monetary mix raises several questions about the Not-So-Great Recovery.

First, would the global recovery have been stronger if fiscal policy had tightened less rapidly than has actually occurred? Since the short term fiscal multiplier is almost certainly not zero, the answer to this question is clearly “yes”, but it is hard to ascribe the whole of the shortfall in GDP growth to this single factor.

If real government expenditure had performed as normal in this recovery, this would have resulted in spending being about 5 percentage points of GDP higher than it is now, so the fiscal multiplier would have needed to be about 2 in order to explain the whole of the 10 per cent growth shortfall. This seems implausibly high. Furthermore, monetary policy would have been tighter in such fiscal circumstances, and there would have been a somewhat greater (if still small) risk of fiscal crises in some economies. Therefore the Not-So-Great Recovery is not just a fiscal story.

Second, if fiscal policy is not the only factor at work, what else has been going on? Here the primary candidate is surely the collapse and subsequent malfunctioning of the banking system. Kenneth Rogoff and Carmen Reinhart, for all their arithmetical faults, warned that this would be the case, and it has been. Furthermore, the fact that the US repaired its banking system more rapidly than Europe probably explains a good part of the earlier recovery in US private spending in 2012/13. The US/Europe divergence on growth is often attributed entirely to the difference in fiscal policy between the two continents, which means that the difference in bank reform all too easily gets forgotten.

Third, if global fiscal policy is tightening and the European banking sector is still in deep trouble, can a continuation of balance sheet expansion by the central banks produce a stronger recovery? The IMF and its economists seem to be answering “yes” to this question, since they are forecasting much stronger global growth in 2014 and 2015.

But there must surely be severe doubts about this conclusion. Both the IMF and the major central banks are becoming concerned that quantitative easing is causing excessive risk taking in some financial assets, and it is doubtful whether the beneficial effect on the wider economy, via price expectations and aggregate demand, is as powerful as it was at the start.

Conclusion

The IMF’s conclusion is familiar enough: less fiscal tightening should take place in the US this year, along with longer term fiscal reform; root and branch restructuring and recapitalisation of the European banking sector is essential; and monetary accommodation is still needed because it is the only game in town. A familiar message, but this week there was little sign that any of the major policy-makers were listening.

Posted by at 10:29 PM

Labels: Forecasting Forum

Subscribe to: Posts