Tuesday, July 3, 2012

How Vulnerable Is Sweden’s Housing Market?

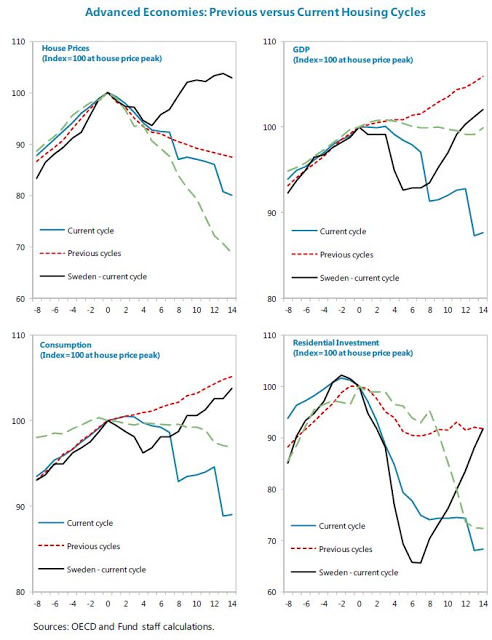

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value. Indeed, in the two years to 2011 Q2, residential investment (+37 percent) took off again, contrary to more muted developments during the previous recovery, offsetting the sharp drop in new homebuilding experienced during the global crisis.

Going forward, several factors may indicate further downward pressure on house prices. First, price-to-income and price-to-rent ratios remain 1.1 and 1.4 standard deviations respectively above historical averages. Second, staff’s model-based estimates from the Early Warning Exercise (EWE) and Vulnerability Exercise for Advanced Countries (VEA) suggest an overvaluation around 11–12 percent, exceeding the 10 percent threshold. (The EWE real estate model combines these three indicators to create a heat map for house price valuation.) Moreover, the predicted path of house prices based on WEO income projections suggests a decline of almost 5-6 percent through 2017.

These indicators put Sweden among the advanced countries where a house price correction is most likely to take place. Yet, the point estimate for the house price disequilibrium (the difference between actual prices and estimated equilibrium or long-run prices) is not large by historical standards, and Sweden ranks only 9th among 22 advanced economies in the VEA sample in terms of potential overvaluation. Furthermore, other components of residential real estate vulnerability (namely, potential impact on GDP, household balance sheets, and mortgage market characteristics) remain moderate or low in Sweden, compared to other advanced economies. That said, with most mortgages being “rollover” mortgages with terms of at most five years, any future interest rate increases could put additional strains on already highly indebted households.

Posted by at 2:24 PM

Labels: Global Housing Watch

Subscribe to: Posts