Friday, February 10, 2012

House Prices in Singapore

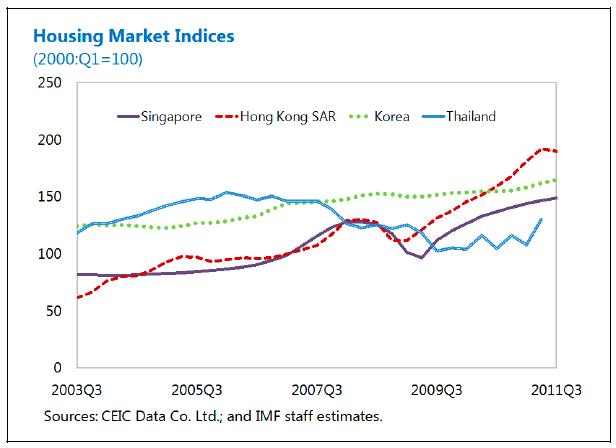

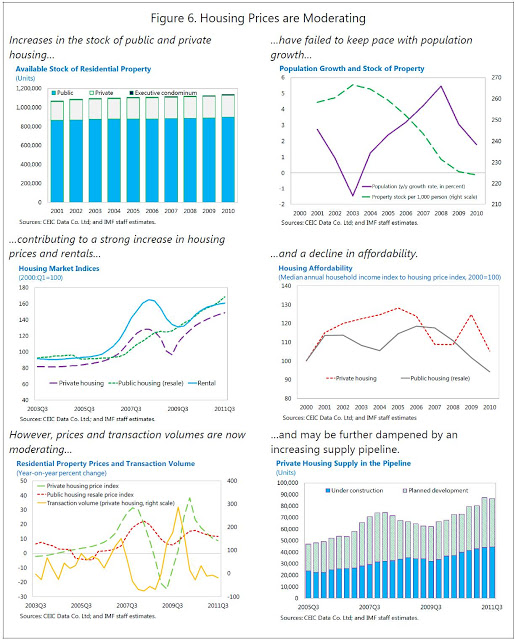

“Following a steep decline in 2008−09, private residential property prices rebounded strongly and are now above the previous peak. Public housing resale prices, which were more resilient during the crisis, are also growing rapidly, and this has allowed many owners to sell and upgrade into private housing, contributing to price pressures in that market. House prices have outpaced median household incomes, leading to a decline in home affordability, which has become a prominent social issue.

Property prices have been propelled by:

- A resurgent economy, which has buoyed incomes.

- Low interest rates. Real mortgage rates have been very low or negative for the past two years, leading to high housing credit growth rates.

- Supply constraints. Housing supply has not kept pace with population growth, which has been driven up by strong immigration.

- Demand by nonresidents. A booming economy and prospects of currency appreciation, along with Singapore’s strong investment climate, have lured foreign interest in the housing market.

Between September 2009 and January 2011, the authorities adopted four rounds of measures to contain demand, including the introduction (and subsequent tightening) of seller stamp duties, and lowering of LTV caps on private property loans. In a fifth round in December 2011, they introduced an additional buyer’s stamp duty, aimed at curbing investment demand, particularly from foreigners and corporate. The authorities have also undertaken measures to increase the supply of public and private housing

Staff analysis suggests that the measures undertaken by the authorities through January 2011 have helped contain prices and transaction volumes in the housing market, both of which are now moderating. Along with slower domestic growth, an uncertain outlook, and a significant supply pipeline of public and private housing projects (although residential construction activity is slowing), the housing market was already likely to cool further. The latest measures in December 2011 took markets by surprise and shifted the balance of risks further downward. Because these measures are residency˗based and focus on the housing market, they also carry some risk of pushing foreign demand over to commercial and industrial property markets (which are also experiencing price increases) or to other countries.”

Posted by at 10:02 PM

Labels: Global Housing Watch

Subscribe to: Posts