Thursday, February 2, 2012

House Prices in Norway

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

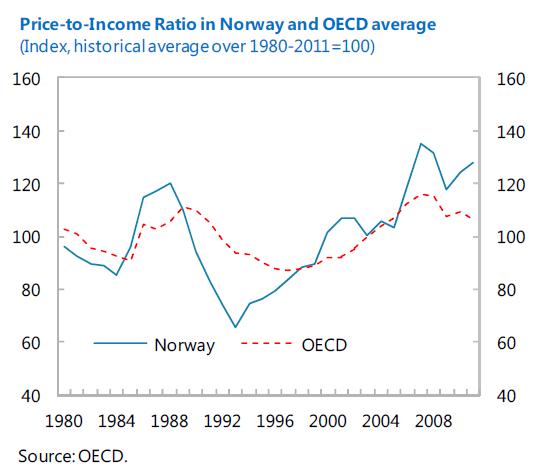

- The house price-to-income ratio has also been rising. This ratio is now 28 percent above its historical average—higher than the peak reached before the last major house price bust in Norway two decades ago.

- While fundamentals explain part of the boom, signs also point to risks of overvaluation. On balance, model based estimates from the IMF’s Early Warning Exercise (EWE), which take into account the key determinants of house prices, suggest that Norwegian residential property prices may be misaligned by 15-20 percent. However, there is admittedly a high amount of uncertainty around this estimate in both directions.

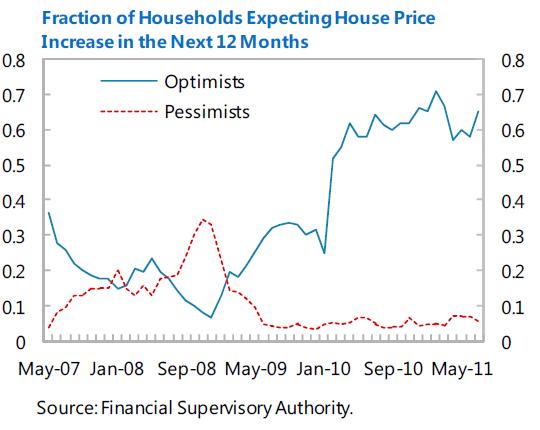

- Expectations of increasing prices may lead agents to buy for speculative motives. An increasing number of households believe that property prices will continue to appreciate. (…) Today, 70 percent of the survey respondents expect price to increase over the next 12 months.

- Another candidate for explaining the boom is loose credit conditions. (…) the share of mortgages with loan-to-value (LTV) ratios over 90 percent has been high since data were first collected in the late 1990s, after the boom was already underway. However, it is somewhat worrisome that the share of mortgages with LTVs over 90 percent has increased since 2010, despite the issuance of FSA guidelines recommending against allowing LTVs to exceed this level, other than in exceptional circumstances.

- About 95 percent of mortgages loans are adjustable-rate and interest payments are front-loaded, low interest rates have made mortgages cheaper and homes significantly more affordable.

- Total household mortgage debt as a fraction of disposable income has increased to 195 percent by end-2010.

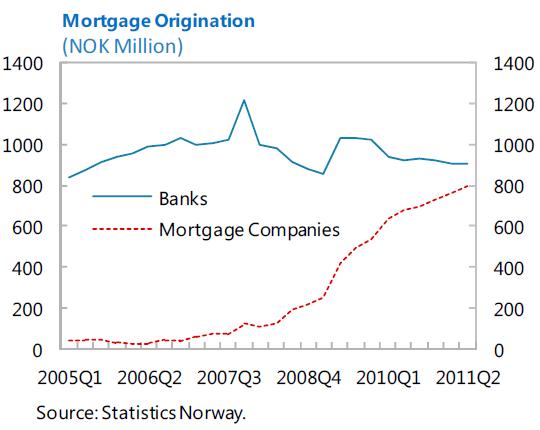

- The volume of secured loans issued by mortgage companies has picked up considerably since 2008. In 2011, loans from mortgage companies represented nearly 50 percent of new mortgages.

- Owner-occupied housing receives quite generous tax treatment in Norway.

- A house price bust would likely be associated with depressed economic activity and increased financial sector stress, especially given high levels of mortgage debt.

- The estimates suggest that a 10 per cent drop in real house prices in Norway is associated with roughly 1 percentage point lower GDP growth than otherwise. (…) A correction of 30 percent in house prices—as occurred during the crisis in the 90s—would exert a non-negligible effect to the real economy.

Posted by at 3:36 PM

Labels: Global Housing Watch

Subscribe to: Posts