Tuesday, December 20, 2011

Housing Market in Korea

An interesting paper by my IMF colleagues Deniz Igan and Heedon Kang looks at how limits on loan-to-value ratios and debt-to-income ratios affect the housing market in Korea.

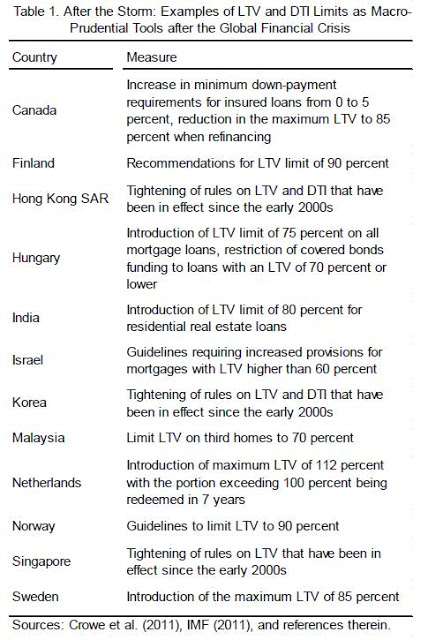

“Prior to the crisis, when it came to dealing with asset price booms, the widely-accepted tenet was one of ‘benign neglect’, namely, to wait for the bust and pick up the pieces (Bernanke and Gertler, 2001). Yet, the crisis and its formidable costs shifted the balance to the opposite camp favoring pre-emptive policy actions that could stop bubbles or, at least, could contain the damage to the financial sector and the broader economy when the bust comes. In other words, many policymakers now think that it is better to act than wait on the sidelines because the cost of inaction may greatly exceed the potential negative side effects of policy intervention. (…) In the quest to better design the policy toolkit to deal with real estate booms and busts, macroprudential tools such as maximum limits on loan-to-value ratios (LTV) and debt-to-income ratios (DTI) are heavily advocated. This has led several countries to recently adopt such limits or measures that would discourage high-LTV/DTI loans.”

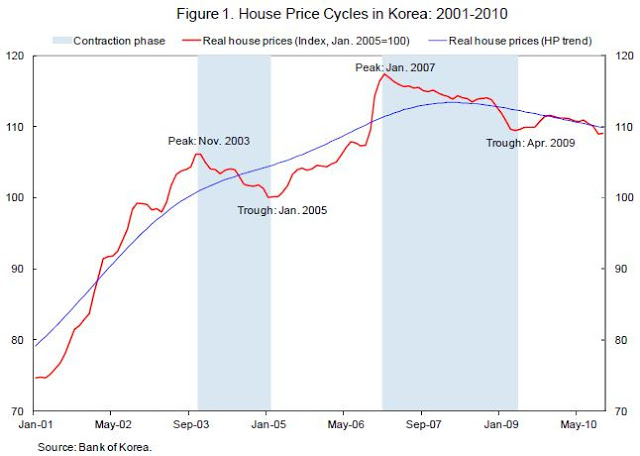

Korea is one of a dozen countries that have adopted such limits.

“we know little about the impact of these measures that have become popular with many regulators after the crisis. Theoretically, limits on LTV and DTI can kill two birds with one stone: they can curb the feedback loop between mortgage credit availability and house price appreciation, and, by restraining household leverage, they can help reduce the incidence and loss given default of residential mortgage loan delinquencies.”

The paper asks two questions

“First, what happens when LTV/DTI limits are adjusted in response to developments perceived to be risky? Second, can we quantify the impact of LTV and DTI limits on housing and mortgage activity?”

What are their conclusions? Igan and Kang find that

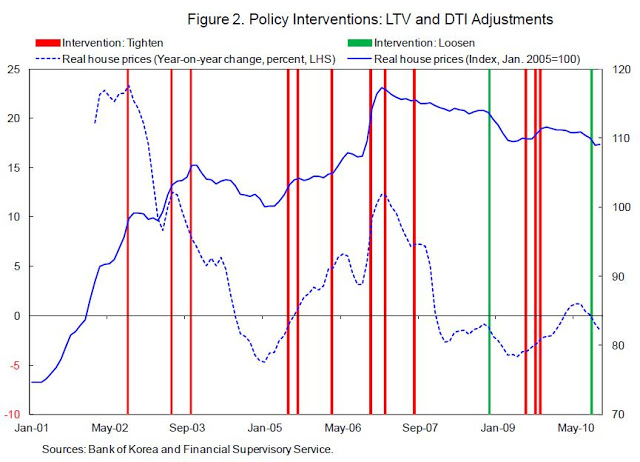

“transaction activity drops significantly in the three-month period following the tightening of LTV/DTI regulations. Price appreciation slows down a bit later, in a six-month window rather than the three-month window. Moreover, price dynamics appear to be reined in more after LTV tightening rather than DTI tightening. [The authors provide evidence for what the] channel for the impact of the policy actions may be: expected house price increases in the future become lower after policy intervention and this is more prevalent among older households while plans to purchase of a home are more likely to be postponed by those who already own a property, i.e., potential speculators, but not by those who do not own a property, i.e., potential first-time home buyers. These findings suggest that tighter limits on loan eligibility criteria, especially on LTV, curb expectations and speculative incentives. Policy implications of our analysis are encouraging. In housing markets, expectations are key as they often facilitate the settling in of bubble dynamics. If, as suggested by the evidence presented here, limits on LTV curb expectations and discourage potential speculators, they can be effective tools to tame real estate booms and contain the associated risks.”

Posted by at 10:08 PM

Labels: Global Housing Watch

Subscribe to: Posts