Showing posts with label Inclusive Growth. Show all posts

Wednesday, March 23, 2022

Will COVID-19 Have Long-Lasting Effects on Inequality? Evidence from Past Pandemics

From a new paper by Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto:

“This paper provides evidence on the impact of major epidemics from the past two decades on income distribution. The pandemics in our sample, even though much smaller in scale than COVID-19, have led to increases in the Gini coefficient, raised the income share of higher income deciles, and lowered the employment-to-population ratio for those with basic education compared to those with higher education. We provide some evidence that the distributional consequences from the current pandemic may be larger than those flowing from the historical pandemics in our sample, and larger than those following typical recessions and financial crises.”

From a new paper by Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto:

“This paper provides evidence on the impact of major epidemics from the past two decades on income distribution. The pandemics in our sample, even though much smaller in scale than COVID-19, have led to increases in the Gini coefficient, raised the income share of higher income deciles, and lowered the employment-to-population ratio for those with basic education compared to those with higher education.

Posted by at 12:24 PM

Labels: Inclusive Growth

Sunday, March 20, 2022

An assessment of US labor market rigidity

Source: VoxEU CEPR

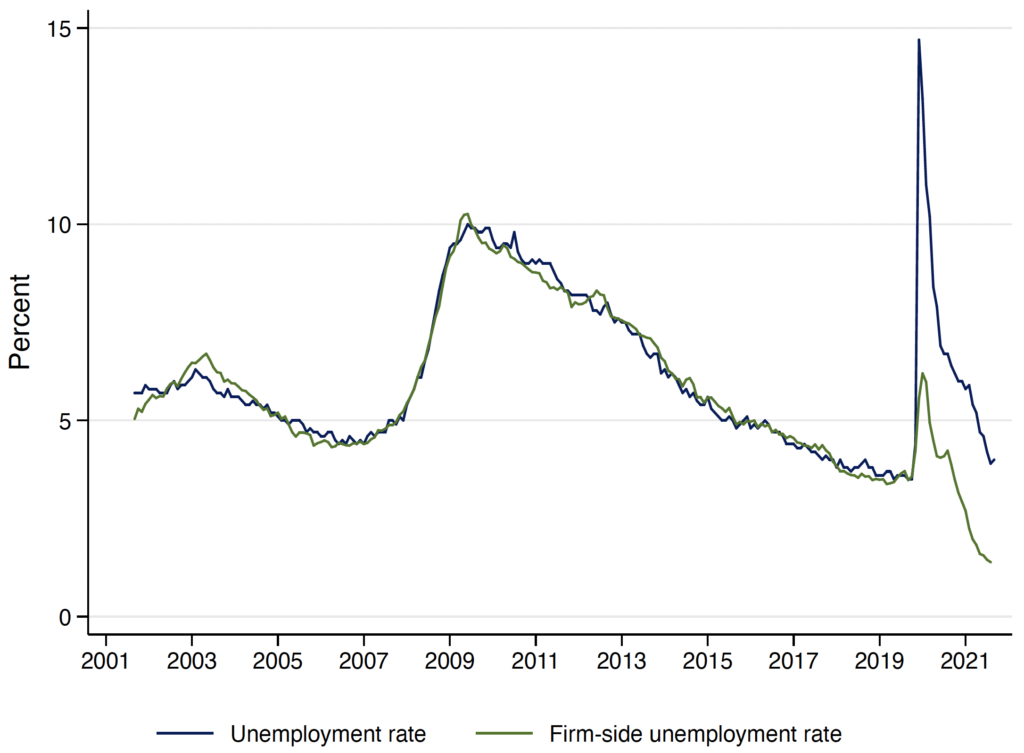

Abstract: Since the beginning of the pandemic, labour market indicators have been sending different signals about the degree of slack in the US labour market. This column uses time-series and cross-section data to show that firm-side unemployment (figure underneath) – a measure that ties together the unemployment rate with the vacancy and quits rate – predicts wage inflation better than the unemployment rate or the employment ratio, and that firm-side unemployment currently experienced in the US corresponds to a degree of tightness previously associated with sub 2% unemployment. The findings suggest that labour markets in the US are extremely tight and will likely contribute to inflationary pressures for some time to come.

Figure: Actual unemployment rate versus firm-side estimated unemployment rate

Source: VoxEU CEPR

Abstract: Since the beginning of the pandemic, labour market indicators have been sending different signals about the degree of slack in the US labour market. This column uses time-series and cross-section data to show that firm-side unemployment (figure underneath) – a measure that ties together the unemployment rate with the vacancy and quits rate – predicts wage inflation better than the unemployment rate or the employment ratio,

Posted by at 10:58 AM

Labels: Inclusive Growth

Monday, March 14, 2022

Tackling Gender Gaps in Data

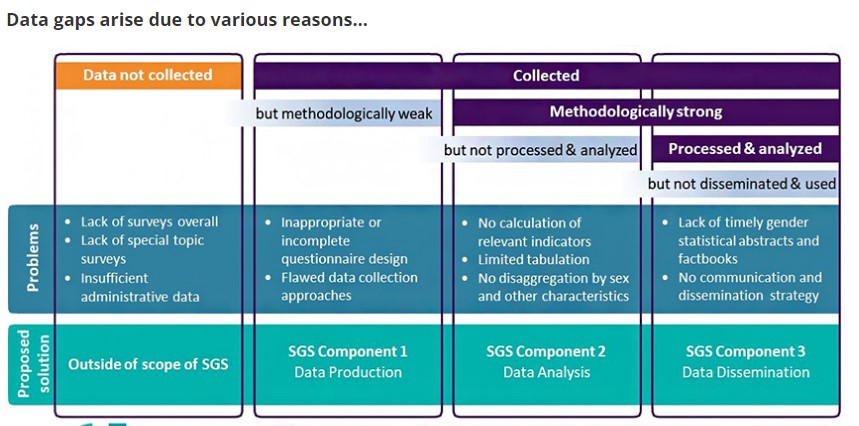

Ironically, in the big data age of today, a significant barrier to women’s inclusion in formal economies is made up of the lack of sex-disaggregated data at the high level. Within this, the lack of more granular data to base models and policies on, the lack of data on related services like internet access, use of bank accounts, feature phones and smartphones, or even inclusion in the national identification process is hard to come by.

In a recent blog detailing ideas for their new project, Strengthening Gender Statistics, officials from the World Bank Group write about challenges to accessing quality gendered data and how to tackle them. They try to understand the vast variety of challenges by grouping them into three categories- challenges to data production, analysis, and dissemination.

Read also:

Making Women and Girls Visible: Gender Data Gaps and Why They Matter (2018), UN Women

Closing gender data gaps in the world of work- role of the 19th ICLS standards (2020), ILO

Ironically, in the big data age of today, a significant barrier to women’s inclusion in formal economies is made up of the lack of sex-disaggregated data at the high level. Within this, the lack of more granular data to base models and policies on, the lack of data on related services like internet access, use of bank accounts, feature phones and smartphones, or even inclusion in the national identification process is hard to come by.

Posted by at 3:07 PM

Labels: Inclusive Growth

Thursday, March 10, 2022

Does evidence-based policymaking always work?

Source: Ideas for India

In a recent column for the Ideas for India blog, development economist Jean Dreze writes about the perils of experimental policymaking. While data-based policy design is quite the rage now with randomized control trials (RCTs) being used to gather evidence on “what works” and then scaling up whatever does, Dreze writes how a more comprehensive approach to policymaking would be one where insights from data are interspersed with a sound mix of understanding the issues, value judgments, and deliberation on inclusivity.

He makes a case for this argument by discussing an experiment conducted in the Indian state of Bihar during 2012-13 to study a new financial management system in the Mahatma Gandhi National Rural Employment Guarantee Act (Banerjee, Duflo, Imbert, Mathew, and Pande (2020). From delivering counter-productive results in the form of reducing, not enhancing, the baseline expenditure on this scheme to delays in workers’ payments and the lack of significant differences between outputs of the treatment and control groups, this article draws attention to the challenges associated with hasty rollouts of interventions and subsequent conclusions based on them without negating the learnings. It concludes with some best practices for engaging with governments, conducting experiments at scale, and ensuring that the “do no harm” principle of RCTs stays put.

Source: Ideas for India

In a recent column for the Ideas for India blog, development economist Jean Dreze writes about the perils of experimental policymaking. While data-based policy design is quite the rage now with randomized control trials (RCTs) being used to gather evidence on “what works” and then scaling up whatever does, Dreze writes how a more comprehensive approach to policymaking would be one where insights from data are interspersed with a sound mix of understanding the issues,

Posted by at 1:19 PM

Labels: Inclusive Growth

Monday, March 7, 2022

Learning from the East Asian Urbanization Model

Source: Centre for Global Development

For the many urbanized and rapidly urbanizing countries, the East Asian experience with and response to emerging challenges is a model to look up to. As high-income East Asian economies approach peaking urbanization, they are now plagued with several challenges. From service sector and export-led growth outstripping manufacturing to rising carbon levels in cities, aging populations, and infrastructure that struggles to catch up with advances in technology- the concerns are aplenty.

In this working paper for the think tank, CGDEV, author Shahid Yusuf writes about how EA countries can respond to these challenges with the use of strategic long-range planning, technological advances, broader implementation capacity, and better resource mobilization. With that, he draws larger inferences that can guide policymakers in tackling the challenges of urbanization elsewhere.

Source: Centre for Global Development

For the many urbanized and rapidly urbanizing countries, the East Asian experience with and response to emerging challenges is a model to look up to. As high-income East Asian economies approach peaking urbanization, they are now plagued with several challenges. From service sector and export-led growth outstripping manufacturing to rising carbon levels in cities, aging populations, and infrastructure that struggles to catch up with advances in technology- the concerns are aplenty.

Posted by at 10:37 AM

Labels: Inclusive Growth

Subscribe to: Posts