Tuesday, December 10, 2019

Housing Market in Cyprus

From the IMF’s latest report on Cyprus:

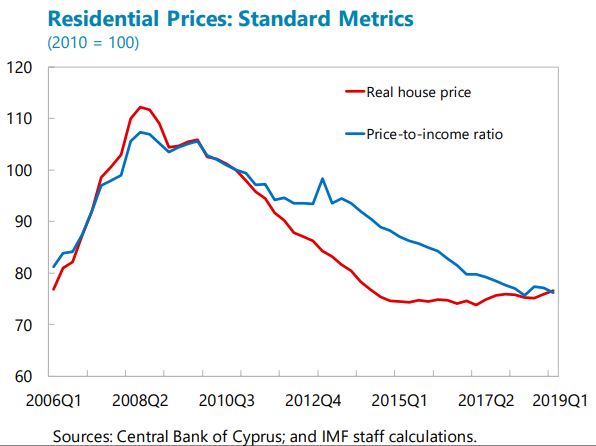

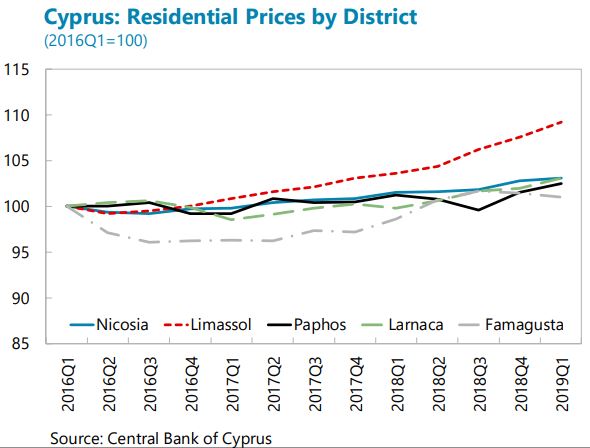

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented, however, with higher price increases observed primarily in a growing luxury segment in some coastal areas (e.g., Limassol), fueled by the CIP-linked demand from non-residents, with limited spillovers to other segments so far. Rents have been rising rapidly—17 percent in 2018— mainly driven by the growing demand from foreign students and lagging supply of rental property investments, prompting the authorities to increase rental and housing subsidies and a range of incentives for developers to increase supplies of affordable housing and rental properties.

Macro-financial risks from the property market appear limited now but warrant close monitoring. While the sales of repossessed collateral properties by banks and CACs could potentially depress prices, downward pressures from such sales have not been evident in any market segments. However, it is important to continue monitoring sectoral and regional real estate market developments, considering the segmented nature of the market. Macroprudential measures tailored to the market segment should be undertaken if warranted, e.g. if the luxury sales become associated with rapid credit growth or high loan-to-value ratios. On the supervisory front, continued monitoring is needed on the large holdings of repossessed real estate by banks and CACs, to discourage and limit the risk of excessive holding of foreclosed properties. Also, the increased real estate holding by investment funds warrants close monitoring to mitigate risks related to liquidity mismatches. Supervisory tools, in particular Pillar 2 requirements and explicit bank-specific objectives, should continue to be used to discourage excessive holding of foreclosed properties by banks.”

From the IMF’s latest report on Cyprus:

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented,

Posted by at 11:01 AM

Labels: Global Housing Watch

Monday, December 9, 2019

China’s Productivity Convergence and Growth Potential—A Stocktaking and Sectoral Approach

Interesting research paper by Min Zhu , Longmei Zhang and Daoju Peng:

“China’s growth potential has become a hotly debated topic as the economy has reached an income level susceptible to the “middle-income trap” and financial vulnerabilities are mounting after years of rapid credit expansion. However, the existing literature has largely focused on macro level aggregates, which are ill suited to understanding China’s significant structural transformation and its impact on economic growth. To fill the gap, this paper takes a deep dive into China’s convergence progress in 38 industrial sectors and 11 services sectors, examines past sectoral transitions, and predicts future shifts. We find that China’s productivity convergence remains at an early stage, with the industrial sector more advanced than services. Large variations exist among subsectors, with high-tech industrial sectors, in particular the ICT sector, lagging low-tech sectors. Going forward, ample room remains for further convergence, but the shrinking distance to the frontier, the structural shift from industry to services, and demographic changes will put sustained downward pressure on growth, which could slow to 5 percent by 2025 and 4 percent by 2030. Digitalization, SOE reform, and services sector opening up could be three major forces boosting future growth, while the risks of a financial crisis and a reversal in global integration in trade and technology could slow the pace of convergence.”

Interesting research paper by Min Zhu , Longmei Zhang and Daoju Peng:

“China’s growth potential has become a hotly debated topic as the economy has reached an income level susceptible to the “middle-income trap” and financial vulnerabilities are mounting after years of rapid credit expansion. However, the existing literature has largely focused on macro level aggregates, which are ill suited to understanding China’s significant structural transformation and its impact on economic growth.

Posted by at 1:57 PM

Labels: Inclusive Growth

A Look at Housing Affordability in Asia

Global Housing Watch Newsletter: December 2019

In this interview, Matthias Helble talks about the state of housing affordability in Asia, the causes and consequences of worsening housing affordability, and policies to address housing affordability issues. Matthias is an Economist in the Economic Research and Regional Cooperation Department at the Asian Development Bank.

On the state of housing affordability

Hites Ahir: In the latest issue of the Asian Development Outlook, you talk about affordable housing in the region. What is the state of housing affordability?

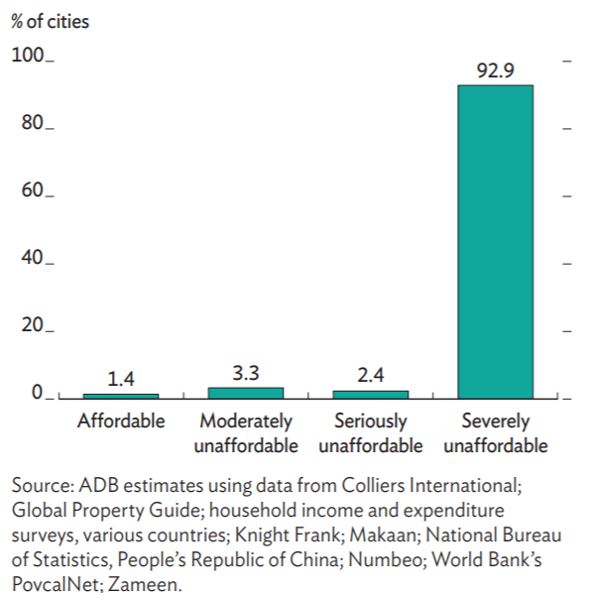

Matthias C. Helble: The state of housing affordability looks very dire. We collected detailed housing price data from public and private sources for 211 cities in 27 countries in developing Asia. Combining them with household income data, we calculated the price-to-income ratio (PIR) by city. Our results show that on average the PIR is 15.6, indicating that housing is severely unaffordable. The unaffordability is not only limited to large cities (with more than 5 million inhabitants), but also affects smaller cities (with less than 1 million inhabitants). Furthermore, we cannot see systematic differences across subregions in Asia. Cities in all subregions suffer equally, be it in Central Asia, East Asia, South East Asia, South Asia, or the Pacific. The housing unaffordability stretches from West to East, from Karachi, Kathmandu, Dhaka, and Bangkok to Dili (Timor-Leste), and from South to North starting from Jakarta, Ha Noi, and Vientiane, to Beijing and Ulaanbaatar.

Figure 1: Housing affordability in 211 cities in 27 countries in Asia

HA: How do you measure housing affordability?

MH: We measure housing affordability by the price-to-income ratio (PIR), which is probably the most commonly used indicator of housing affordability. It is the ratio of the housing unit price over the annual median household income. Demographia International suggests the following cut-offs: A PIR of below 3 is considered to indicate affordable housing. Housing is moderately unaffordable if the PIR is 3 to 4. For example, cities in developed countries have a PIR averaging 4.0. If the PIR is above 4.1, housing is considered seriously unaffordable, and a PIR above 5 indicates that housing is severely unaffordable. In our sample of 211 cities, we only found three cities (Hubli Dharwad in India, Khulna in Bangladesh, and Timphu in Bhutan) that have affordable housing.

HA: The level of income in a city tends to be higher than in the rest of the country. Do you think the results might be overstating the deterioration of housing affordability in the region?

MH: It is indeed a challenge to obtain household income data at the city-level. For several countries, we had access to household income and expenditure surveys (HIES) at the city-level (or a geographical unit that was dominated by a single city). We could thus control for the fact that the level of income is higher in cities. For the remaining countries in our sample, we made use of the positive relationship between city size and income and adjusted the national household income upward using a regression-based approach. Apart from the challenge of adjusting national household income to city size, the HIES data itself might not always accurately report the entire income of a household. An underreporting of household income would lead to an overstatement of the housing affordability problem. In order to test the sensitivity of our results, we developed various scenarios, for example assuming that the real household income was 25 percent higher. Running these tests, we found that housing remained severely unaffordable in most cities in our sample because the housing prices are simply very high.

On the causes and consequences

HA: What is driving the deterioration in housing affordability?

MH: The main driver is the rapid urbanization in Asia, alongside economic success. The demand for housing is thus increasing rapidly while the supply is lagging. Cities have been slow in expanding the availability of low-cost developable land with access to public amenities and transport. The land price of well-served and centrally located areas is thus spiraling. At the same time, we see a lot of unplanned, even chaotic, urban expansion. Another aggravating factor is that in Asia almost everybody aspires to become a homeowner and the rental market is still relatively small in most cities in developing Asia.

HA: What does the literature say about the consequences of a deterioration in housing affordability?

MH: The unaffordability of housing has severe consequences beyond the negative impact on the individual household. Housing unaffordability damages the economic competitiveness of cities and thus can undermine the growth prospects of the entire country. We have solid empirical evidence of three main channels through which housing unaffordability affects the economy:

- First, housing unaffordability results in a less flexible labor market and thus leads to labor misallocation.

- Second, as housing prices rise, firms tend to invest in real estate rather than in innovation and productivity enhancement. Furthermore, banks tend to lend more to firms that have real estate assets instead of the best business prospects, resulting in capital misallocation.

- Third, high housing prices deter people from moving to the city. Housing unaffordability thus slows the process of urbanization and thereby reduces agglomeration-induced productivity growth and aggregate welfare.

On the cures

HA: What policies have been implemented in Asia?

MH: A wide range of policies have been tried throughout Asia. The table below provides some examples. It is important not to expect that the same housing policy would work equally across countries. For example, an idle land tax boosted the construction of housing after the Second World War. The same policy today is not having much effect in the Philippines due to uncertain land titles.

Table 1: Main policy options used in Asia toward affordable housing

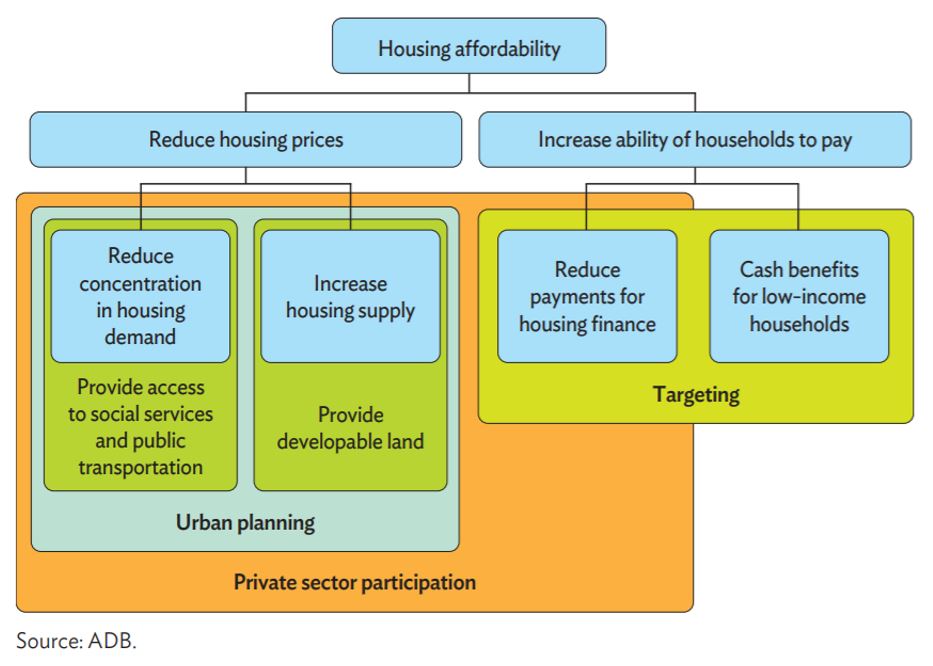

HA: Is there a framework that policymakers can use to address housing affordability issues?

MH: There is no specific framework, rather we have some recommendations.

- First, the housing unaffordability crisis cannot be solved by the public sector alone. The private sector needs to be part of the solution, notably through the provision of low-cost housing. Governments need to provide incentive schemes to encourage that.

- Second, the best housing policies will flounder if the policy implementation and enforcement is weak. This has been the case in many developing countries.

- Finally, we are living in an age in which an incredible amount of data on the housing market and related issues is becoming available. Collecting and analyzing the data and feeding the results into the policy process could greatly improve the effectiveness of housing policies.

Figure 2: Housing policy option tree

HA: Do you think that most of the discussion on affordable housing tends to be around “increasing housing supply” and not concentrating much on other important elements such as affordable transport, upgrading slums, and others? Please explain your opinion.

MH: Increasing housing supply alone will certainly not solve the problem. Similar to other policy areas, there is insufficient coordination between the line ministries responsible for housing and other ministries. Housing policies need to be well embedded into urban planning. Integrated neighborhoods need to be developed with access to social services, such as education and healthcare, as well as transport. Another problem is that we do not yet have enough sound evidence on many aspects of housing prices such as how access to transport affects housing prices in developing countries. Thanks to the emergence of big data, I am convinced that a lot of new interesting insights will soon be uncovered. At the Asian Development Bank, we are already working with big data to measure traffic congestion and travel time, for example.

HA: Is there a success story that you could share with us?

MH: A case that is often cited is Singapore. Yet there are other less well-known, but still very valuable, examples, such as in South Korea. Due to fast economic growth in the 1980s, South Korea witnessed a sharp increase in housing prices in its major cities. The government responded by announcing the “Two-Million Housing Drive,” promising to build 2 million new housing units within 5 years. It achieved the objective through a mix of public and private action. The government also introduced a successful policy of allocating housing units to target income groups according to their ability to pay. This approach improved housing conditions, both in terms of quantity and quality, and helped the middle class to build their wealth through house ownership. The country’s housing policy was also well integrated into urban planning so supply constraints were quickly removed. While certainly not without challenges, South Korea provides a useful example of how to tackle housing affordability.

Global Housing Watch Newsletter: December 2019

In this interview, Matthias Helble talks about the state of housing affordability in Asia, the causes and consequences of worsening housing affordability, and policies to address housing affordability issues. Matthias is an Economist in the Economic Research and Regional Cooperation Department at the Asian Development Bank.

On the state of housing affordability

Hites Ahir: In the latest issue of the Asian Development Outlook,

Posted by at 5:00 AM

Labels: Global Housing Watch

Views from housing market experts

This page compiles together 31 interviews with housing market experts. The interviews are organized by different topics.

On housing market developments across countries

- Enrique Martínez-García and Valerie Grossman (Federal Reserve Bank of Dallas), August 2016.

- Gabriela Inchauste (World Bank), February 2019.

- Ian Bright and Jessica Exton (ING), November 2018.

- Kate Everett-Allen (Knight Frank), September 2017.

- Marja C Hoek-Smit (HOFINET), March 2016.

- Paul Cheshire (London School of Economics), March 2019.

- Stephen Malpezzi (University of Wisconsin-Madison), March 2017.

On housing markets in Africa

- Issa Faye, El-Hadj M. Bah, and Zekebweliwai F. Geh (African Development Bank), April 2018.

- Kecia Rust (Centre for Affordable Housing Finance in Africa), February 2017 and November 2017.

- Riël C. D. Franzsen (University of Pretoria), October 2017.

On housing market in the US and other countries

- Frank Nothaft (CoreLogic, US), August 2017.

- Issi Romem (BuildZoom, US), July 2016.

- Keyes Christopher “KC” Hardin (Conservatorio SA, Panama), September 2018.

- Sock-Yong Phang (Singapore Management University, Singapore), April 2018.

On housing affordability

- Albert Saiz (Massachusetts Institute of Technology), September 2018.

- Matthias Helble (Asian Development Bank), November 2019.

- Shlomo Angel and Achilles Kallergis (New York University), September 2016.

- Stijn Van Nieuwerburgh (Columbia University), September 2019.

- Svenja Gudell (Zillow), October 2016.

On housing finance

- Sarah Quinn (University of Washington) November 2019.

- Susan Wachter (University of Pennsylvania), May 2019.

On housing policies

- Lars E.O. Svensson (Stockholm School of Economics), June 2015.

- Matthias Helble (Asian Development Bank Institute), November 2016.

- Nora Libertun de Duren [In Spanish] (Inter-American Development Bank), March 2018.

- Paavo Monkkonen ( University of California, Los Angeles), March 2018.

On housing supply

- Daniel Garcia (Federal Reserve Board) October 2019.

- Jan Mischke (McKinsey Global Institute), June 2017.

- Jordan Rappaport (Federal Reserve Bank of Kansas City), May 2017 .

- Joseph Gyourko (University of Pennsylvania), April 2017.

On globalization of housing markets

- Christian Hilber (London School of Economics), July 2018.

- Richard Ronald (University of Amsterdam), July 2017.

This page compiles together 31 interviews with housing market experts. The interviews are organized by different topics.

On housing market developments across countries

- Enrique Martínez-García and Valerie Grossman (Federal Reserve Bank of Dallas), August 2016.

- Gabriela Inchauste (World Bank), February 2019.

- Ian Bright and Jessica Exton (ING), November 2018.

- Kate Everett-Allen (Knight Frank), September 2017.

Posted by at 4:00 AM

Labels: Global Housing Watch

Friday, December 6, 2019

Local Capital Scarcity and Small Firm Growth: Evidence from Real Estate Booms in China

From a working paper by Harald Hau, and Difei Ouyang:

“In geographically segmented credit markets, local real estate booms can deteriorate the funding conditions for small manufacturing firms and undermine their competitiveness. Using exogenous variation in the administrative land supply across 172 Chinese cities, we show that higher predicted real estate prices cause higher borrowing costs for small manufacturing firms, reduce their bank lending, lower their investment rate and labor productivity, and reduce their output and TFP growth by economically significant magnitudes. These effects are absent in large and listed companies with access to the national capital market. The evidence highlights the benefits of financial market integration.”

From a working paper by Harald Hau, and Difei Ouyang:

“In geographically segmented credit markets, local real estate booms can deteriorate the funding conditions for small manufacturing firms and undermine their competitiveness. Using exogenous variation in the administrative land supply across 172 Chinese cities, we show that higher predicted real estate prices cause higher borrowing costs for small manufacturing firms, reduce their bank lending, lower their investment rate and labor productivity,

Posted by at 5:17 PM

Labels: Global Housing Watch

Subscribe to: Posts