Monday, June 17, 2019

Managing House Price Booms: Evolution of IMF Surveillance and Policy Advice

This chapter describes the evolution of IMF monitoring—“surveillance” in the IMF’s jargon—of housing markets from 2008 to the present. It explains how the IMF has assessed overvaluation in housing markets and the advice offered on the policy tools needed to manage house price booms. The IMF’s ‘corporate view’ or ‘house view’ that macroprudential policies must be the first line of defense to deal with house price booms is laid out. The chapter also discusses whether the run-up in house prices over the past few years should be a source of worry. Lastly, the chapter describes how IMF surveillance has adapted as housing markets have become more ‘glocalized’ and developments at the sub-national level gain greater prominence.

In April 2008, the IMF’s flagship publication World Economic Outlook provided estimates of overvaluation in house prices for a group of advanced economies. Though house prices had fallen in the United States in the preceding years, they had continued to rise in many other countries. The IMF’s analysis suggested that, with only a few exceptions, house prices were overvalued by between 10% and 30%, as shown by the bars in Fig. 7.1. The dots show the decline in house prices that occurred over the subsequent 4 years. In many countries where the IMF had assessed house prices to be overvalued, house prices did indeed fall quite significantly—these cases include Denmark, Ireland, the Netherlands and the United Kingdom.

Fast forward to the present: The IMF’s Global House Price Index—a simple average of real house prices for 57 countries—is now back to its level before the global financial crisis (GFC). The index has been inching up since 2012, making the duration of the run-up comparable to one in 2001–06 that ended in house price collapses in many countries. Is it time to worry again about overvaluation?

Read the rest of chapter here and the book here.

This chapter describes the evolution of IMF monitoring—“surveillance” in the IMF’s jargon—of housing markets from 2008 to the present. It explains how the IMF has assessed overvaluation in housing markets and the advice offered on the policy tools needed to manage house price booms. The IMF’s ‘corporate view’ or ‘house view’ that macroprudential policies must be the first line of defense to deal with house price booms is laid out. The chapter also discusses whether the run-up in house prices over the past few years should be a source of worry.

Posted by at 11:08 AM

Labels: Global Housing Watch

The return of the policy that shall not be named: Principles of industrial policy

From VoxEU post by Reda Cherif and Fuad Hasanov:

“The ‘Asian miracles’ and their industrial policies are often considered as statistical accidents that cannot be replicated. The column argues that we can learn more about sustained growth from these miracles than from the large pool of failures, and that industrial policy is instrumental in achieving sustained growth. Successful policy uses state intervention for early entry into sophisticated sectors, strong export orientation, and fierce competition with strict accountability.

Achieving sustained growth over long periods of time has been an elusive ‘holy grail’ of macroeconomics. In the past 50 years developing economies have taken different paths. A few – such as the ‘Asian miracles’ of Hong Kong (China), South Korea, Singapore, and Taiwan Province of China – are catching up swiftly with the advanced economies, and some forging ahead. But many are falling behind, to use the terminology of Abramovitz (1986).

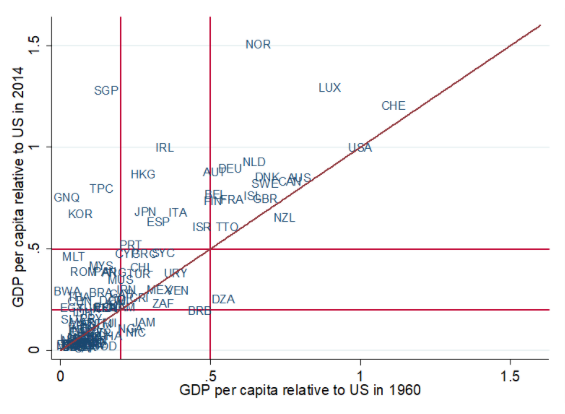

The empirical evidence shows that the odds for poor or middle-income countries to reach high-income status within two generations are very low (Cherif and Hasanov, forthcoming). Between 1960 and 2014, fewer than 10% of economies (16 out of 182 in the sample) reached high-income status. There were three categories of those that made it: Asian miracles, countries that discovered large quantities of oil, and those that benefited from joining the European Union (Figure 1)

Figure 1 Half a century of development

Source: Penn World Tables 9.0 (Feenstra et al. 2015).

Note: GDP per capita is in 2011 PPP dollars. The thresholds for upper-middle income and high income are 20 % and 50% of US GDP per capita, respectively (red lines). The diagonal line indicates no change in relative income levels (with respect to the US level).We argue (Cherif and Hasanov 2019) that one cannot ignore the pre-eminent role of industrial policy in the development of the Asian miracle countries as well as for Japan, Germany, and the US before them. The industrial policies pursued by the Asian miracles have a lot in common. This suggests that the standard ‘growth policy recipe’ of tackling only government failures (improving macro-stability, enforcing property rights, providing basic infrastructure and education, and so on) may not be enough to create advanced economies in a short period of time. Instead, recent research suggests that industrial policy may benefit economic development too (Rodrik 2019).”

From VoxEU post by Reda Cherif and Fuad Hasanov:

“The ‘Asian miracles’ and their industrial policies are often considered as statistical accidents that cannot be replicated. The column argues that we can learn more about sustained growth from these miracles than from the large pool of failures, and that industrial policy is instrumental in achieving sustained growth. Successful policy uses state intervention for early entry into sophisticated sectors, strong export orientation,

Posted by at 10:37 AM

Labels: Inclusive Growth

Housing Market in Ireland

From the IMF’s latest report on Ireland:

“Unlike during the pre-crisis period, rising housing prices have not been fueled by excessive credit but rather by a lagging supply response to rising demand. Robust job creation, rising wages, low interest rates, and population growth have all contributed to a strong recovery in housing demand since 2013. The supply of housing, however, has not kept pace. The main factors that have prevented a faster expansion in housing supply are constraining regulations, weaknesses in the zoning and planning process, financial difficulties of construction firms, skills shortages in the construction sector, and land hoarding.

The government has taken several measures to increase housing supply, develop the rental market, and improve affordability.1 The Rebuilding Ireland Action Plan for Housing and Homelessness, announced in July 2016, seeks to double the annual level of residential construction to 25,000 homes by 2020, deliver an additional 50,000 social housing units in the period to 2021, and meet the housing needs of an additional 87,000 households through housing assistance schemes. Home Building Finance Ireland, a newly established state lender for financially constrained developers, aims to deliver up to 7,500 new homes over the next five years, financed by a €750 million investment from the Ireland Strategic Investment Fund. Other initiatives include an infrastructure fund designed to provide local public infrastructure to facilitate housing development, and a new fast-track planning process for large-scale housing developments.

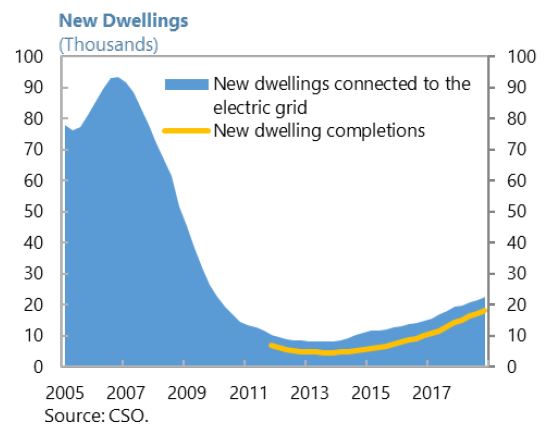

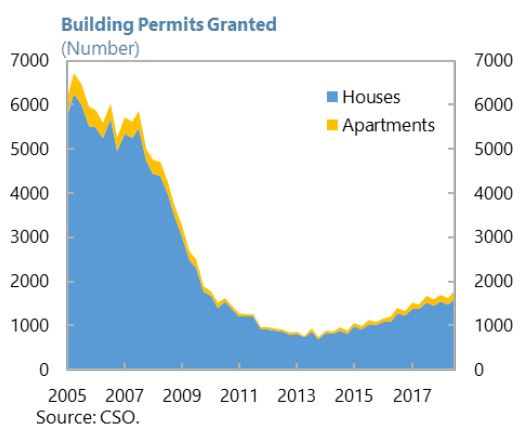

There are indications that the housing supply will continue to expand. The number of new dwellings connected to the electric grid increased by 17 percent in 2018—the fifth consecutive year of growth, albeit from a low base—while new dwelling completions have also grown rapidly. Forward-looking indicators point to further growth. Building permits granted for the construction of houses and apartments increased by 8.5 percent year-on-year in 2018:Q3, and employment continues to increase in the construction sector.”

From the IMF’s latest report on Ireland:

“Unlike during the pre-crisis period, rising housing prices have not been fueled by excessive credit but rather by a lagging supply response to rising demand. Robust job creation, rising wages, low interest rates, and population growth have all contributed to a strong recovery in housing demand since 2013. The supply of housing, however, has not kept pace. The main factors that have prevented a faster expansion in housing supply are constraining regulations,

Posted by at 10:30 AM

Labels: Global Housing Watch

Friday, June 14, 2019

Some Snapshots of the Global Energy Situation

From Conversable Economist:

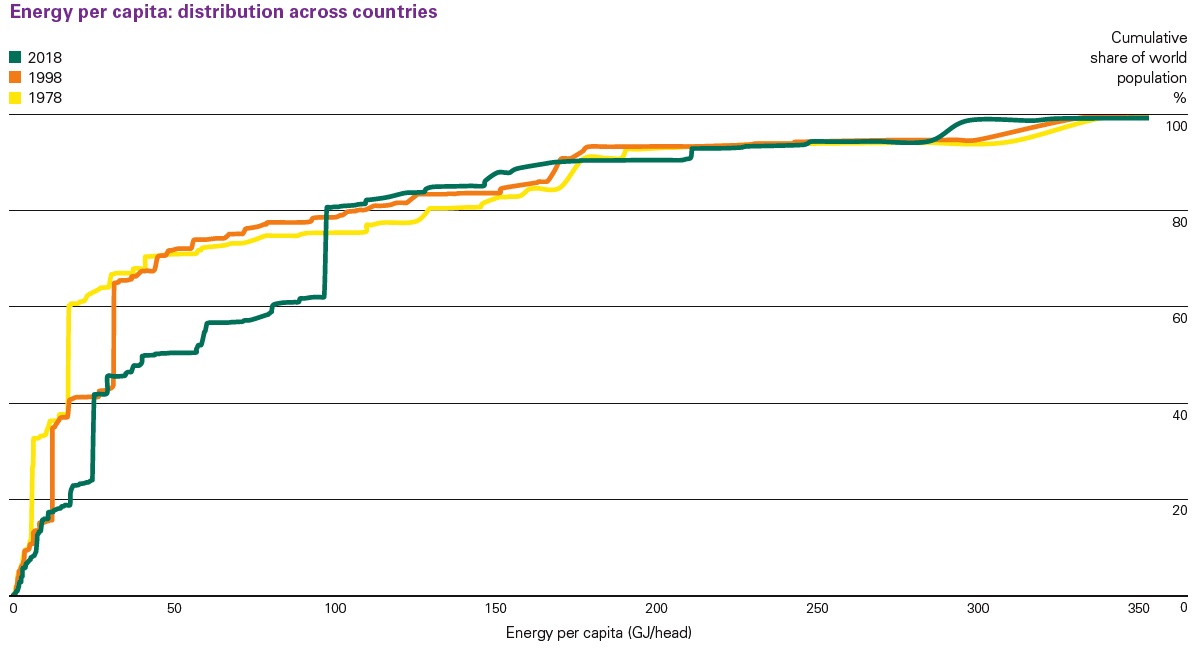

“Global primary energy grew by 2.9% in 2018 – the fastest growth seen since 2010. This occurred despite a backdrop of modest GDP growth and strengthening energy prices. At the same time, carbon emissions from energy use grew by 2.0%, again the fastest expansion for many years, with emissions increasing by around 0.6 gigatonnes. That’s roughly equivalent to the carbon emissions associated with increasing the number of passenger cars on the planet by a third.” Spencer Dale offers these and other insights in his introduction to the the 2019 BP Statistical Review of World Energy. It’s one of those books of charts and tables I try to check each year just to keep my personal perceptions of economic patterns connected to actual statistics. Here are a few figures that jumped out at me.

One main drive of the rise in world energy use is economic growth in emerging market countries. The horizontal axis of this figure shows average energy use per person. The vertical axis shows the cumulative share of total world population. The yellow line shows the pattern for 1978, while the green line shows four decades later in 2018.”

Continue reading here.

From Conversable Economist:

“Global primary energy grew by 2.9% in 2018 – the fastest growth seen since 2010. This occurred despite a backdrop of modest GDP growth and strengthening energy prices. At the same time, carbon emissions from energy use grew by 2.0%, again the fastest expansion for many years, with emissions increasing by around 0.6 gigatonnes. That’s roughly equivalent to the carbon emissions associated with increasing the number of passenger cars on the planet by a third.”

Posted by at 2:46 PM

Labels: Energy & Climate Change

Thursday, June 13, 2019

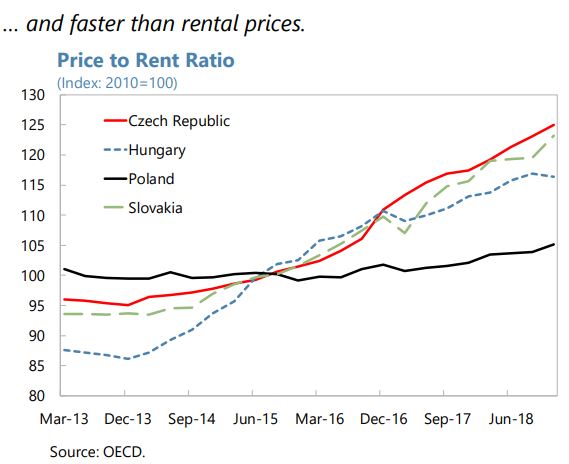

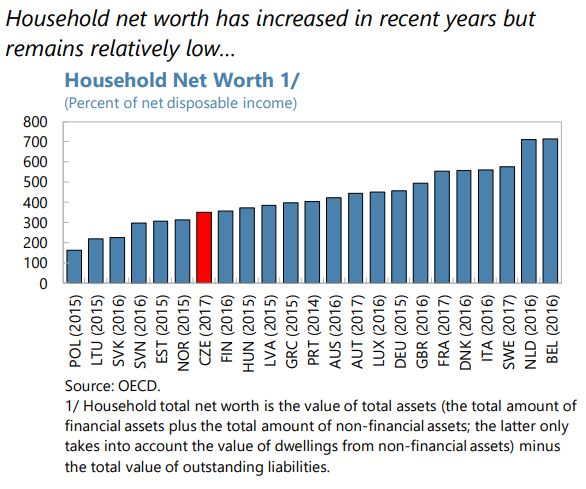

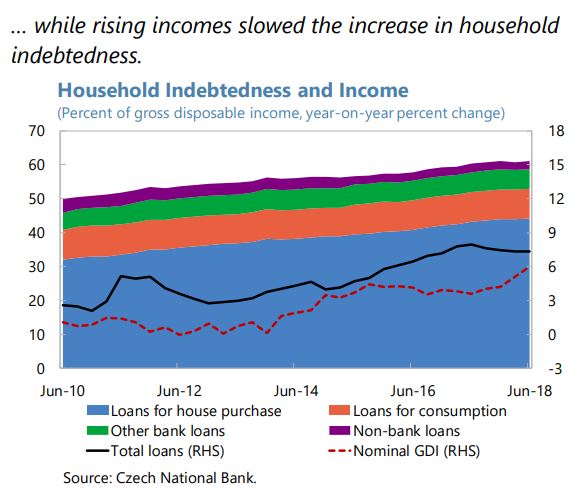

Housing Market in Czech Republic

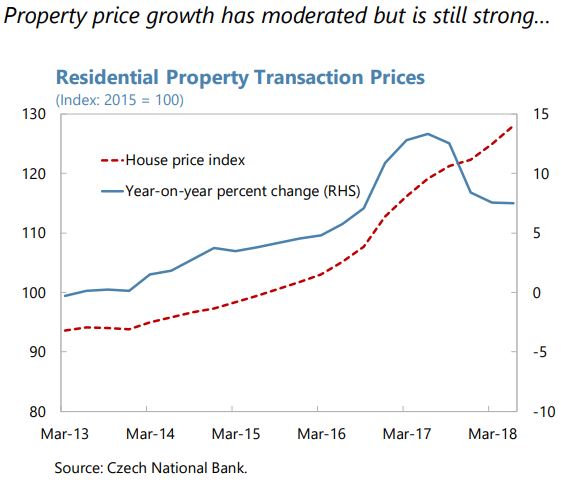

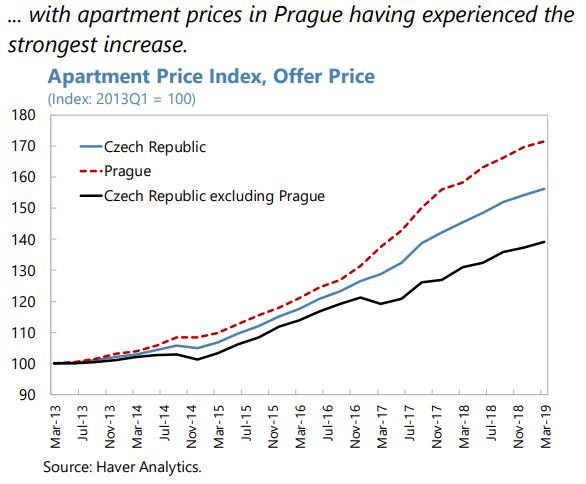

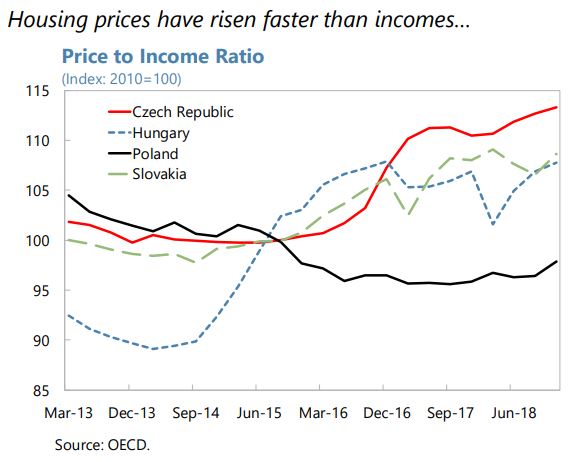

From the IMF’s latest report on Czech Republic:

“The housing market remains pressured.

Despite a recent deceleration, house price growth was still among the 5 highest in the EU in 2018, outpacing wage and income growth (Figure 7). In Prague, where most property transactions take place, offered prices for apartments have increased by 44 percent in the three years from 2016 to 2018. The price-to-income ratio has increased by a cumulative 12.6 percent between 2015: Q4 and 2018: Q4, after having been stable over the preceding 5 years. House price increases have also made a substantial contribution to the measure of CPI targeted by the CNB.

Private nonfinancial sector credit accelerated from the previous year, growing ahead of nominal incomes. This was driven primarily by mortgage credit, which continues to grow at a high rate (…). But new mortgage volumes are decreasing amid increasing lending rates and tighter macroprudential borrower recommendations. Nonfinancial corporate lending growth also increased in 2018.”

From the IMF’s latest report on Czech Republic:

“The housing market remains pressured.

Despite a recent deceleration, house price growth was still among the 5 highest in the EU in 2018, outpacing wage and income growth (Figure 7). In Prague, where most property transactions take place, offered prices for apartments have increased by 44 percent in the three years from 2016 to 2018. The price-to-income ratio has increased by a cumulative 12.6 percent between 2015: Q4 and 2018: Q4,

Posted by at 2:40 PM

Labels: Global Housing Watch

Subscribe to: Posts