Wednesday, May 17, 2017

Every Woman Counts: Gender Budgeting in G7 Countries

From IMF direct by Managing Director Christine Lagarde:

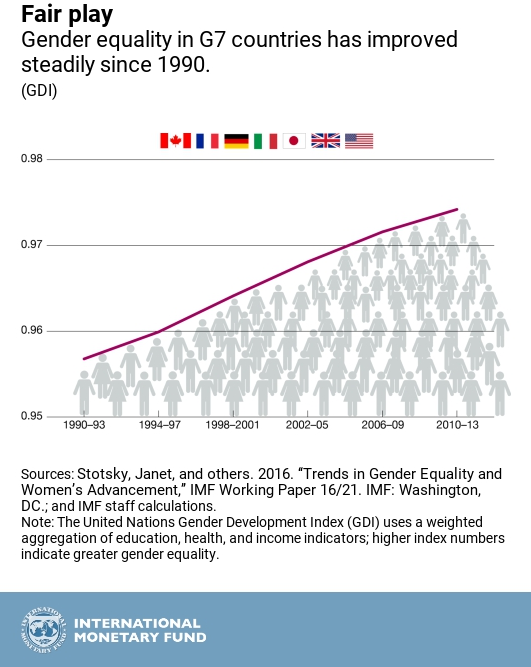

“(…) despite progress made by most G7 countries in improving gender equality (see chart below), there is still a large unfinished agenda. For example, in advanced industrial countries, women’s labor market participation rate is about 17 percentage points lower than men’s. The wage gap between women and men amounts to roughly 14 percent. The share of male managers is almost double that of women, and almost 70 percent of unpaid work is performed by women.

The point I was making to the G7 countries is that, to make further progress, national budgets can be used more actively as a tool to support gender equality. For example, in advanced economies, tax policies play an important role in addressing disincentives for secondary earners to work. Spending policies can help too, for instance by supporting childcare facilities. One example is the Canadian child benefit scheme, which helps families with the cost of childcare through a tax-free, income-tested benefit. This and other examples are listed in the table below.”

Continue reading here.

From IMF direct by Managing Director Christine Lagarde:

“(…) despite progress made by most G7 countries in improving gender equality (see chart below), there is still a large unfinished agenda. For example, in advanced industrial countries, women’s labor market participation rate is about 17 percentage points lower than men’s. The wage gap between women and men amounts to roughly 14 percent. The share of male managers is almost double that of women,

Posted by at 6:36 PM

Labels: Inclusive Growth

Monday, May 15, 2017

Belt and Road Initiative: Strengthening Financial Connectivity

IMF Managing Director Christine Lagarde quoted my research with Davide Furceri during her speech: “IMF analysis shows that having a more inclusive financial system makes it safer—and more beneficial—to relax restrictions on capital flows across borders . By liberalizing their capital account over time, countries can attract more foreign investment, increase the liquidity of local financial markets, and reduce their cost of capital. In other words, by developing deep, well-regulated financial markets, countries can better mobilize domestic and international resources for investment—while reducing the financial stability risks that come with large capital inflows.”

IMF Managing Director Christine Lagarde quoted my research with Davide Furceri during her speech: “IMF analysis shows that having a more inclusive financial system makes it safer—and more beneficial—to relax restrictions on capital flows across borders . By liberalizing their capital account over time, countries can attract more foreign investment, increase the liquidity of local financial markets, and reduce their cost of capital. In other words, by developing deep, well-regulated financial markets, countries can better mobilize domestic and international resources for investment—while reducing the financial stability risks that come with large capital inflows.”

Posted by at 9:22 AM

Labels: Inclusive Growth

Wednesday, May 10, 2017

Housing Market in Luxembourg

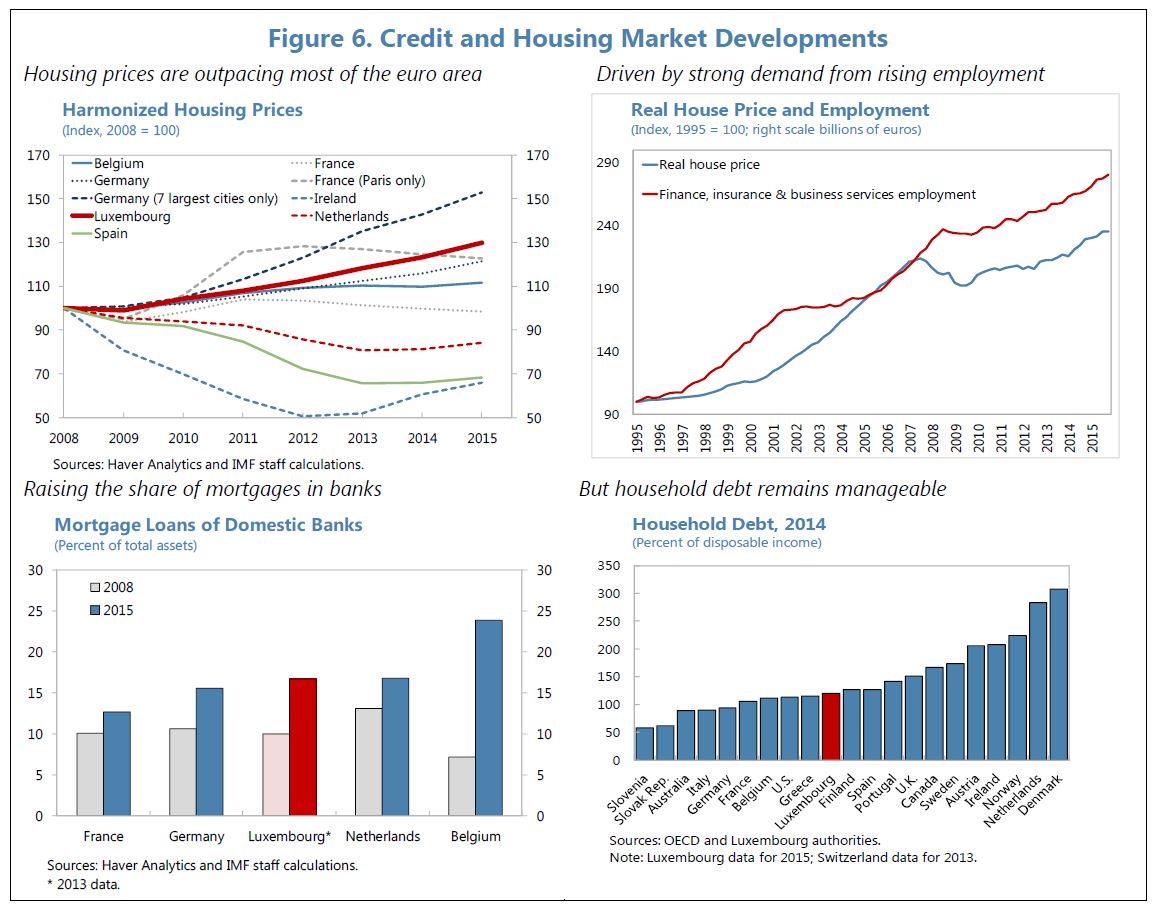

The latest IMF’s report on Luxembourg says: “Against the backdrop of an expanding population, low interest rates and binding supply side constraints, residential real estate price-to-income ratios in Luxembourg have become elevated by historical and global standards (Figure 6). After a marginal decline in 2009, nominal home prices have since increased 30 percent (or 22 percent in real terms), a period over which real disposable income of the local population has been flat, though GDP and employment growth continued.

Supply bottlenecks make housing less affordable to residents. Analysis based on an empirical model of real house prices suggests that real house prices were overvalued before the global financial crisis because house prices were growing significantly faster than a trend (explained by population growth). Since then, their evolution has become more aligned with real GDP and population growth, in spite of the flat disposable income of the resident population while the low interest rate environment has improved their borrowing capacity. This analysis suggests that supply has only partially adjusted to the rapid growth of demand.”

The latest IMF’s report on Luxembourg says: “Against the backdrop of an expanding population, low interest rates and binding supply side constraints, residential real estate price-to-income ratios in Luxembourg have become elevated by historical and global standards (Figure 6). After a marginal decline in 2009, nominal home prices have since increased 30 percent (or 22 percent in real terms), a period over which real disposable income of the local population has been flat,

Posted by at 2:03 PM

Labels: Global Housing Watch

Tuesday, May 9, 2017

The Informal Economy in Sub-Saharan Africa

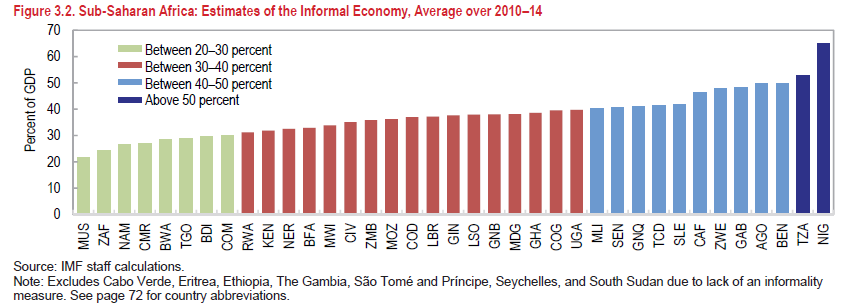

A new IMF Regional Economic Outlook on Sub-Saharan Africa says that “The informal economy is a key component of most economies in sub-Saharan Africa, contributing between 25 and 65 percent of GDP and accounting for between 30 and 90 percent of total nonagricultural employment. While international experience indicates that the share of the informal economy declines as the level of development increases, most economies in sub-Saharan Africa are likely to have large informal sectors for many years to come, presenting both opportunities and challenges for policymakers.”

A new IMF Regional Economic Outlook on Sub-Saharan Africa says that “The informal economy is a key component of most economies in sub-Saharan Africa, contributing between 25 and 65 percent of GDP and accounting for between 30 and 90 percent of total nonagricultural employment. While international experience indicates that the share of the informal economy declines as the level of development increases, most economies in sub-Saharan Africa are likely to have large informal sectors for many years to come,

Posted by at 3:24 PM

Labels: Inclusive Growth

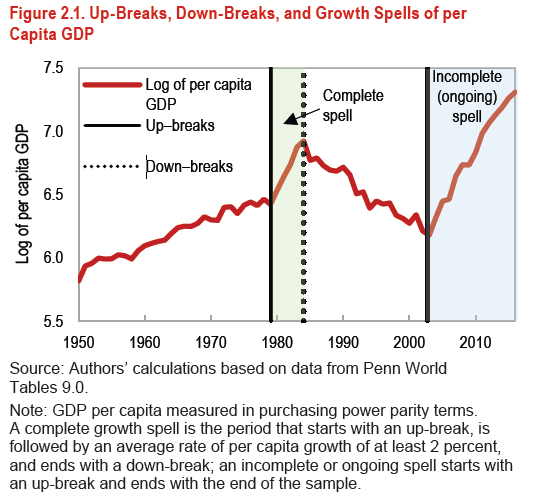

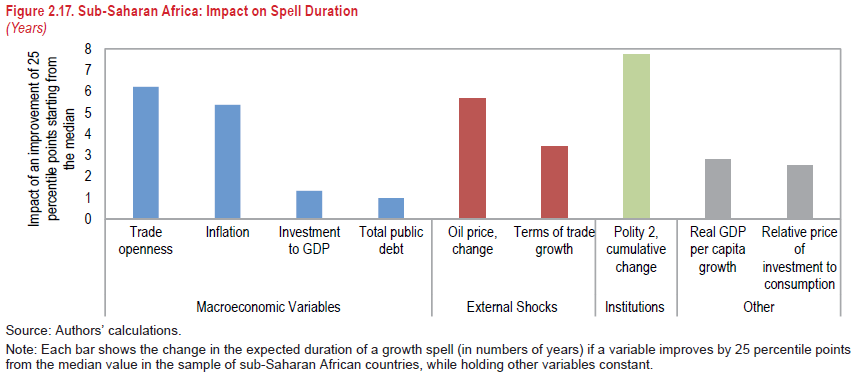

Restarting Sub-Saharan Africa’s Growth Engine

From a new IMF Regional Economic Outlook on Sub-Saharan Africa

“After nearly two decades of strong growth, average economic activity in sub-Saharan Africa has decelerated sharply, against the backdrop of lower commodity prices, a less-supportive global environment, and, in the hardest-hit countries, a delayed policy response (Chapter 1). However, the full picture is more complex, with considerable heterogeneity across countries. Against this backdrop, two related questions arise: How can growth be revived in the hardest-hit countries? And for countries that are still growing fast, how can growth be sustained?

This chapter tries to answer these questions by examining the growth performance of sub-Saharan African countries through the lens of growth turning points and periods of sustained growth episodes using a sample containing data from 1950 to 2016.1 To that effect, the chapter first documents the stylized facts of growth turning points—defined here as growth accelerations (up-breaks) and decelerations (down-breaks)—and sustained growth episodes (growth spells) across the region and vis-à-vis the rest of the world. The chapter then examines the changes in both the external and domestic environment (including policies) that coincided with turning points in sub-Saharan Africa. Finally, the chapter investigates how some episodes of growth acceleration become periods of sustained growth, and what influences the duration of these episodes.”

Continue reading here.

From a new IMF Regional Economic Outlook on Sub-Saharan Africa

“After nearly two decades of strong growth, average economic activity in sub-Saharan Africa has decelerated sharply, against the backdrop of lower commodity prices, a less-supportive global environment, and, in the hardest-hit countries, a delayed policy response (Chapter 1). However, the full picture is more complex, with considerable heterogeneity across countries. Against this backdrop, two related questions arise: How can growth be revived in the hardest-hit countries?

Posted by at 3:14 PM

Labels: Macro Demystified

Subscribe to: Posts