Monday, November 22, 2010

Gloom & Doom … or Boom? The Movie

Here’s the video from a talk at the IMF at which economists Nouriel Roubini (a.k.a. Dr. Doom) and Mark Zandi were pessimistic about the near-term economic outlook but split on how things might look a couple of years from now. Zandi said we might get 5% growth in the US in 2012. Read the full article…

Posted by at 2:42 PM

Labels: Events, Profiles of Economists

The Unemployment Crisis: Costs, Causes, Cures

-

Is the recent increase in unemployment cyclical or structural?

-

Is there is a link between inequality, over-borrowing and financial crises?

My article in The Globalist discusses these issues, among others. The article provides a summary of an October 22 workshop on “The Unemployment Crisis: Costs, Causes, Cures” held at the IMF; the PowerPoint presentations from the workshop are available here. And here’s a link to the final version of my IMF Staff Position Note on “The Human Cost of Unemployment: Assessing It, Reducing It” (with Mai Dao). Three links and I’m out.

-

Is the recent increase in unemployment cyclical or structural?

-

Is there is a link between inequality, over-borrowing and financial crises?

My article in The Globalist discusses these issues, among others. The article provides a summary of an October 22 workshop on “The Unemployment Crisis: Costs, Causes, Cures” held at the IMF; the PowerPoint presentations from the workshop are available here. And here’s a link to the final version of my IMF Staff Position Note on “The Human Cost of Unemployment: Assessing It, Read the full article…

Posted by at 2:09 PM

Labels: Inclusive Growth

Friday, October 15, 2010

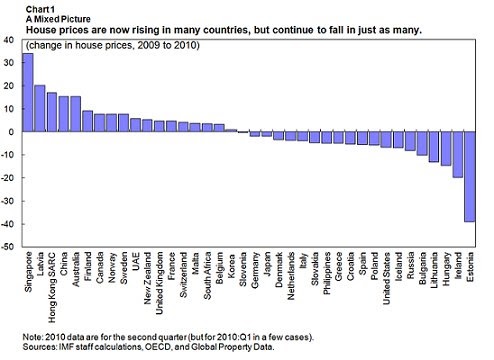

Bouncing Between Floors? Globally, House Prices are Up and Down

Real estate markets have been a source of strength during past economic recoveries, but this time is different. Read the story and see the presentation.

Posted by at 2:38 PM

Labels: Global Housing Watch

Economics Nobel George Akerlof Takes Up Research Position at IMF

If you play a game of word association with an economics Ph.D and say “Akerlof”, chances are the response will be “lemons”. Though best known for his work on the “market for lemons”, Akerlof says the topic that has motivated him the most is unemployment. Read the full story.

If you play a game of word association with an economics Ph.D and say “Akerlof”, chances are the response will be “lemons”. Though best known for his work on the “market for lemons”, Akerlof says the topic that has motivated him the most is unemployment. Read the full story.

Posted by at 2:00 PM

Labels: Profiles of Economists

Wednesday, October 6, 2010

More Room to Fall? Prospects for Housing Markets

The IMF just released its world economic outlook, including this update on the generally dismal prospects for real estate markets across the globe.

Real estate markets have been a source of strength during past recoveries, but this time is different. In many major economies around the globe, house prices continue to fall or are only gradually stabilizing. In a few countries, including the United States, there are concerns of a “double dip” in the housing market. Read the full article…

Posted by at 5:30 PM

Labels: Global Housing Watch

Subscribe to: Posts